EXHIBIT 15.1

Published on March 26, 2024

|

Cadeler A/S. Incorporated in Denmark. Registration Number (CVR no.): 3118 0503 Arne Jacobsens Allé 7, 7. Floor, DK-2300 Copenhagen S, Denmark Annual Report 2023 For the year end 31 December 2023 Cadeler A/S. Incorporated in Denmark. Registration Number (CVR no.): 3118 0503 Kalvebod Brygge 43, DK-1560 Copenhagen V, Denmark |

|

2 Statement from the Chairman and the CEO .........................................................................................3 The Year 2023 in Brief ....................................................................................................................................6 Management Review...................................................................................................................................... 7 Reporting on Sustainability ........................................................................................................................37 Green Finance Report..................................................................................................................................82 Consolidated Financial Statements....................................................................................................... 86 Notes to the Consolidated Financial Statements ............................................................................ 93 Parent Company Financial Statements................................................................................................ 171 Notes to the Parent Company Financial Statements .....................................................................177 Statement by Management..................................................................................................................... 197 Independent Auditor's Report............................................................................................................... 200 Forward-looking Statements..................................................................................................................208 Alternative Performance Measures.......................................................................................................210 ESG Appendices .......................................................................................................................................... 212 Contents |

|

3 As 2023 came to a close, Cadeler secured its place as a global leader in the offshore wind farm transportation and installation industry. Cadeler charted a remarkable course in 2023, showing solid results alongside a stra-tegic scale-up in fleet size, investment in talent, and achievement of a record-breaking backlog of orders. Cadeler is now a global leader in offshore wind farm transportation and installation – ready to achieve its full international potential and to harness the power of wind. The story of the past year has been one of sustained growth for Cadeler – both organi-cally and through the merger with Eneti. This strategic combination, completed in De-cember 2023, made us the world’s leading offshore wind turbine transport and installa-tion company, with a market capitalisation of approximately EUR 1.3 billion, and a dual listing on the Oslo Stock Exchange and New York Stock Exchange. During the year, short-term sentiment around offshore wind turned negative as a result of headlines on some project cancellations, rising interest rates, high inflation and supply chain bottlenecks. However, the market fundamentals remain strong, and Cadeler en-joyed a record year of bookings. Our orderbook now stands at close to EUR 1.7 billion, with a very high percentage of this already at final investment decision stage. Globally, the market will continue to grow at a rapid pace. Offshore wind is a vital ele-ment in the energy transition, and continued geopolitical uncertainty will keep energy se-curity at the top of the international agenda. Cadeler is well positioned for this, due to tight supply of capable offshore wind turbine and foundation installation vessels. Our strategy to serve this expanding sector is to further develop the largest, most diverse and flexible fleet, able to handle complex next-generation offshore projects anywhere in the world. A strong combination of talents After careful consideration of potential partners, Eneti was identified as an ideal strategic fit for Cadeler. Our traditional strength in the European market is complemented by Eneti’s focus on Asia and the United States, creating a combination with full global cov-erage in the installation of next-generation turbines. We are now ready to strategically expand our markets outside Europe, while seeking full utilisation of our vessels. Increased scale and diversification mean that Cadeler will also be able to provide customers with a greater degree of redundancy – lessening the risk of projects falling behind schedule. When bottlenecks occur in the value chain, we can offer a unique flexibility to our clients to address any issues that may arise over the course of the project. We believe the combination with Eneti will deliver around EUR 100 million in annual syn-ergies. This figure comprises corporate and financing savings, such as reduced corpo-rate and management costs, an optimised hiring plan and improved financing terms – and operational synergies, such as cross-utilisation of equipment and better procure-ment efficiency. It also includes utilisation synergies, which will deliver more vessel avail-ability for our clients. Empowering the green transition Cadeler’s commitment to sustainability remains undiminished. In 2023 we have started to explore the uptake of certified biofuels and renewable diesel in our current O-class vessels. These represent a readily available way to reduce emissions from engine com-bustion, replacing fossil fuels and providing our customers with a short-term alternative. Statement from the Chairman and the CEO |

|

4 We were also able to sell the disassembled cranes from our O-class vessels to Hapo In-ternational Barges, granting them a useful second life. Another major focus is on building a fleet of vessels capable of running on alternative fuels in the future. During 2023, significant resources were allocated to ensuring our six newbuild vessels will be ready for eventual conversion to run on alternative fuels. Green methanol has been identified as the option available soonest. However, several fuel pathways have been explored, and we will continue investigating the alternatives during 2024. Furthermore, understanding how energy is consumed on board the vessels is a key driver for Cadeler in improving energy efficiency. During 2023, we continued expanding on our fuel monitoring systems, enabling sufficient real-time data to be utilised to drive im-provement actions. In addition, a heavy focus has been put on delivering newbuild as-sets with a significantly higher level of efficiencies in their design. All these initiatives will form the foundation of a future low-carbon fleet for Cadeler. To help us collaborate and meet the industry’s climate goals, Cadeler joined the EMRED joint industry project led by DNV. This project aims to establish a standardised monitor-ing and reporting framework for assessing greenhouse gas (GHG) emissions in the off-shore wind installation sector, driving emission reductions across the industry. Towards the end of 2023, Cadeler also began its involvement in a project led by Danish Shipping and ReFlow, focused on the development of a digital tool to assess the lifecycle emis-sions of vessels. Finally, we have established a dedicated Decarbonisation and Sustainability department. Sponsored by executive management, it will take responsibility for designing the strat-egy and roadmap for decarbonisation, along with execution and implementation. This strategic decision stemmed from the company’s acknowledgement of the importance and complexity of meeting challenges within these areas. We continue to work towards our long-standing goals of reducing emissions, optimising energy consumption and adopting greener fuels. Embracing change: new people, new fleet When Cadeler rang the bell at the New York Stock Exchange on December 21 last year, marking its listing as a single entity encompassing Eneti, it also welcomed a wealth of new talent on board. The company now employs around 400 seafarers and 230 people onshore. We can proudly say that we offer our business partners access to a talented global team, with continuous improvement in terms of safety, quality and efficiency within offshore wind farm transport and installation services. Whether at the Cadeler headquarters in Copenhagen or at our offices in Vejle in Den-mark, Taipei, Tokyo, Great Yarmouth in the UK or Virginia Beach in the USA, the daily nur-turing and development of our unique Cadeler culture is vital to help unlock industry po-tential – and to accelerate the transition to renewable energy. We will continue to refine our uncompromising “partners first” mentality, where our clients’ success is our guiding star. The Cadeler fleet now numbers four units. The former Eneti vessels Wind Scylla and Wind Zaratan now take their place alongside our existing O-class vessels, Wind Orca and Wind Osprey. Both of the latter units are being upgraded with new state-of-the-art main cranes, with finalisation of installation and commissioning in the early part of 2024. |

|

5 Six newbuild jack-up vessels are on order. Across multiple sites in China, COSCO SHIP-PING Heavy Industry is constructing the two P-class and A-class vessels (previously known as X-class and F-class). The first is set for delivery in Q3 2024, with the others ar-riving throughout 2025. A large team from Cadeler has been supervising the builds, help-ing to ensure quality and safety. An important milestone was recently passed when the projects reached three million person-hours without a lost-time incident (LTI). The two newbuilds ordered by Eneti prior to the merger will add further capability to the fleet. Provisionally named Wind Maker and Wind Mover, these NG16000X jack-up vessels are under construction at Hanwha Ocean in Korea. Their specification includes high-ca-pacity 2,600t cranes, DP2 capability for fast transit between locations, and the ability to operate in water depths of up to 65 metres. Seeking out worldwide potential On the commercial front, highlights of the past year include signing two major contracts with Ørsted for the Hornsea 3 offshore wind farm, with a total value of EUR 500-700 mil-lion. The combined contracts represent the biggest deal in Cadeler’s history, and our first full-service transport and installation contract for foundations. In February 2024, we signed a further transport and installation contract with Ørsted and Polska Grupa Ener-getyczna for the Baltica 2 offshore wind farm in the Baltic Sea. The coming years will see us extend Cadeler’s geographical reach. While our cautious approach to the United States proved to be correct so far, we now hold a more optimis-tic view, and will be involved in the American market this year. We have also identified Asia as a region of interest – especially Taiwan and Korea, which have fast-expanding markets. Our strategy is to move vessels into Asia when there is a real pipeline of work there, rather than doing so on a project-by-project basis. As a global company, we are also continuously looking into other markets, such as South America. A course set for global leadership Looking back on 2023, Cadeler embarked on an extraordinary journey – a course set for global leadership in offshore wind farm transportation and installation. Our ambitions were realised by solid results, a decisive and strategic fleet expansion, continuing invest-ment in talent, and our uncompromising focus on our partners’ success. Cadeler stands ready to harness its full global potential and contribute to the future of renewable off-shore wind energy. Andreas Sohmen-Pao, Chairman of the board Mikkel Gleerup, CEO 5 |

|

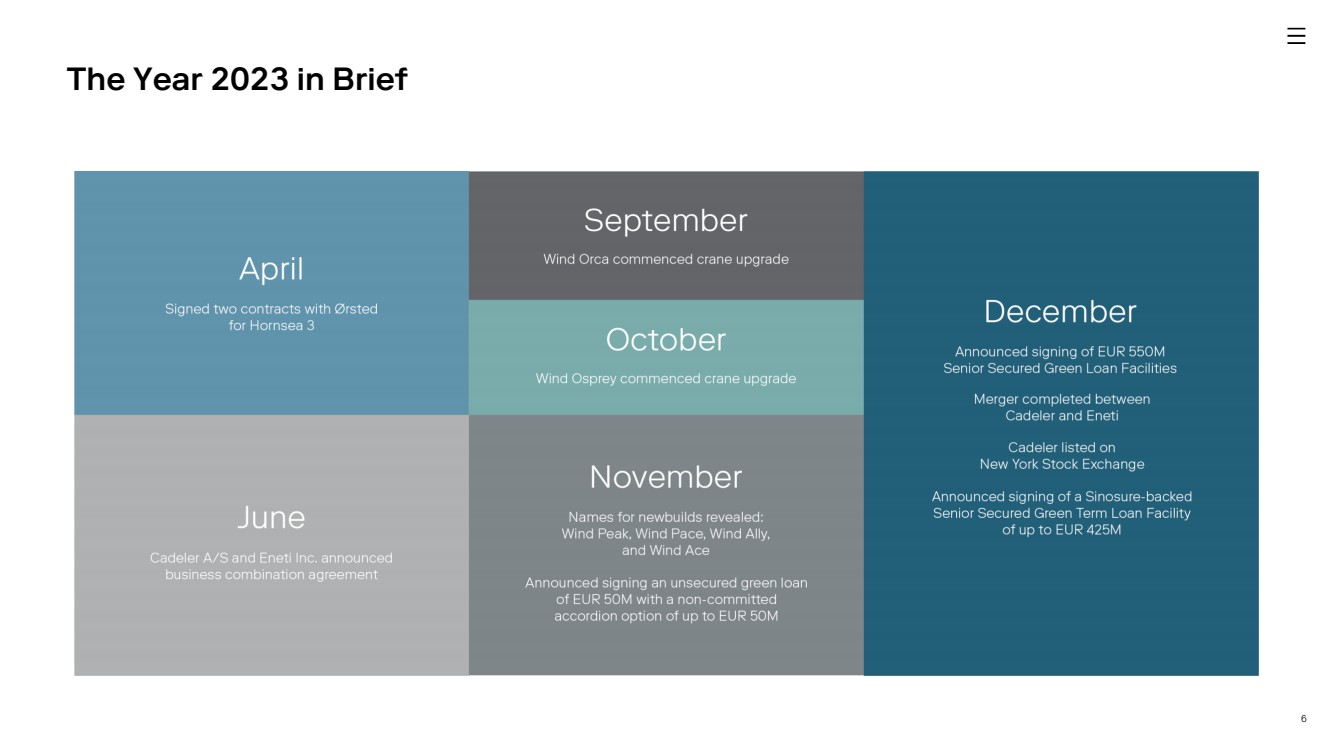

6 The Year 2023 in Brief |

|

7 Management Review 7 |

|

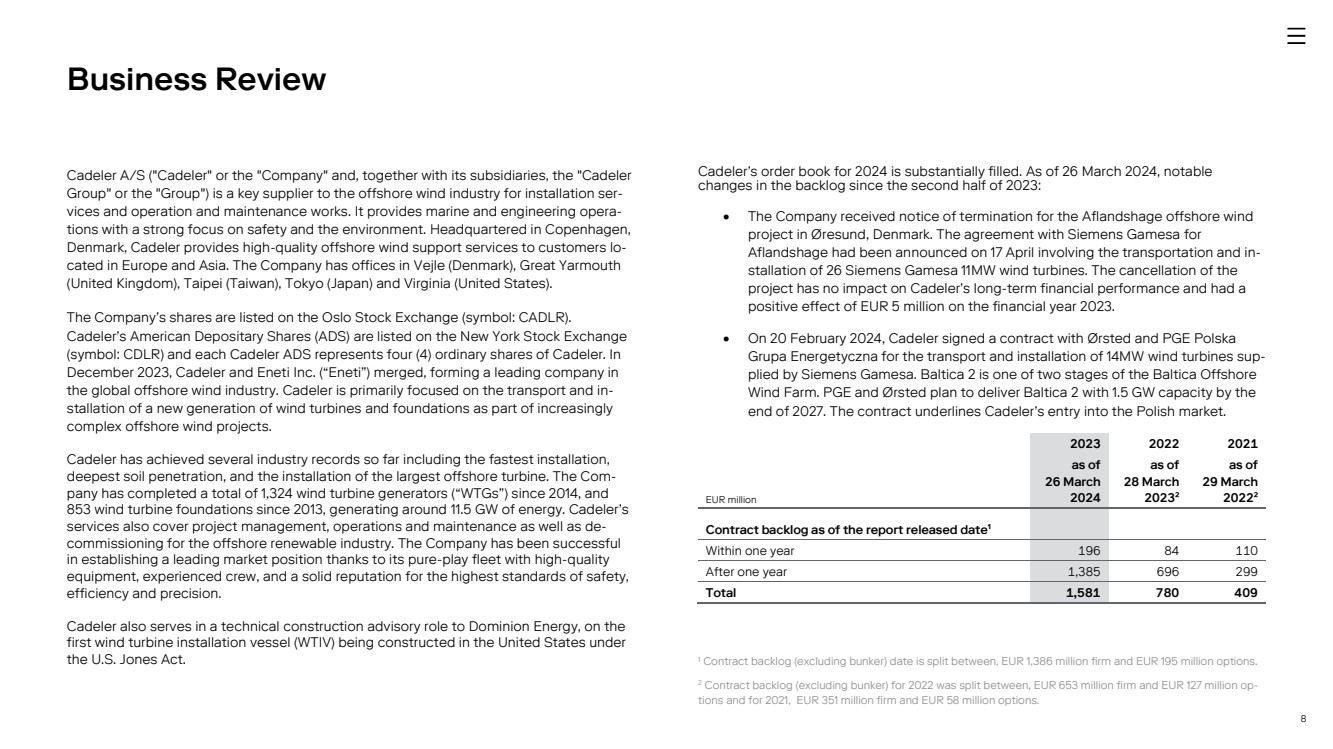

8 Cadeler A/S ("Cadeler" or the "Company" and, together with its subsidiaries, the "Cadeler Group" or the "Group") is a key supplier to the offshore wind industry for installation ser-vices and operation and maintenance works. It provides marine and engineering opera-tions with a strong focus on safety and the environment. Headquartered in Copenhagen, Denmark, Cadeler provides high-quality offshore wind support services to customers lo-cated in Europe and Asia. The Company has offices in Vejle (Denmark), Great Yarmouth (United Kingdom), Taipei (Taiwan), Tokyo (Japan) and Virginia (United States). The Company’s shares are listed on the Oslo Stock Exchange (symbol: CADLR). Cadeler’s American Depositary Shares (ADS) are listed on the New York Stock Exchange (symbol: CDLR) and each Cadeler ADS represents four (4) ordinary shares of Cadeler. In December 2023, Cadeler and Eneti Inc. (“Eneti”) merged, forming a leading company in the global offshore wind industry. Cadeler is primarily focused on the transport and in-stallation of a new generation of wind turbines and foundations as part of increasingly complex offshore wind projects. Cadeler has achieved several industry records so far including the fastest installation, deepest soil penetration, and the installation of the largest offshore turbine. The Com-pany has completed a total of 1,324 wind turbine generators (“WTGs”) since 2014, and 853 wind turbine foundations since 2013, generating around 11.5 GW of energy. Cadeler’s services also cover project management, operations and maintenance as well as de-commissioning for the offshore renewable industry. The Company has been successful in establishing a leading market position thanks to its pure-play fleet with high-quality equipment, experienced crew, and a solid reputation for the highest standards of safety, efficiency and precision. Cadeler also serves in a technical construction advisory role to Dominion Energy, on the first wind turbine installation vessel (WTIV) being constructed in the United States under the U.S. Jones Act. Cadeler’s order book for 2024 is substantially filled. As of 26 March 2024, notable changes in the backlog since the second half of 2023: • The Company received notice of termination for the Aflandshage offshore wind project in Øresund, Denmark. The agreement with Siemens Gamesa for Aflandshage had been announced on 17 April involving the transportation and in-stallation of 26 Siemens Gamesa 11MW wind turbines. The cancellation of the project has no impact on Cadeler’s long-term financial performance and had a positive effect of EUR 5 million on the financial year 2023. • On 20 February 2024, Cadeler signed a contract with Ørsted and PGE Polska Grupa Energetyczna for the transport and installation of 14MW wind turbines sup-plied by Siemens Gamesa. Baltica 2 is one of two stages of the Baltica Offshore Wind Farm. PGE and Ørsted plan to deliver Baltica 2 with 1.5 GW capacity by the end of 2027. The contract underlines Cadeler’s entry into the Polish market. 2023 2022 2021 EUR million as of 26 March 2024 as of 28 March 2023² as of 29 March 2022² Contract backlog as of the report released date¹ Within one year 196 84 110 After one year 1,385 696 299 Total 1,581 780 409 Business Review 1 Contract backlog (excluding bunker) date is split between, EUR 1,386 million firm and EUR 195 million options. 2 Contract backlog (excluding bunker) for 2022 was split between, EUR 653 million firm and EUR 127 million op-tions and for 2021, EUR 351 million firm and EUR 58 million options. |

|

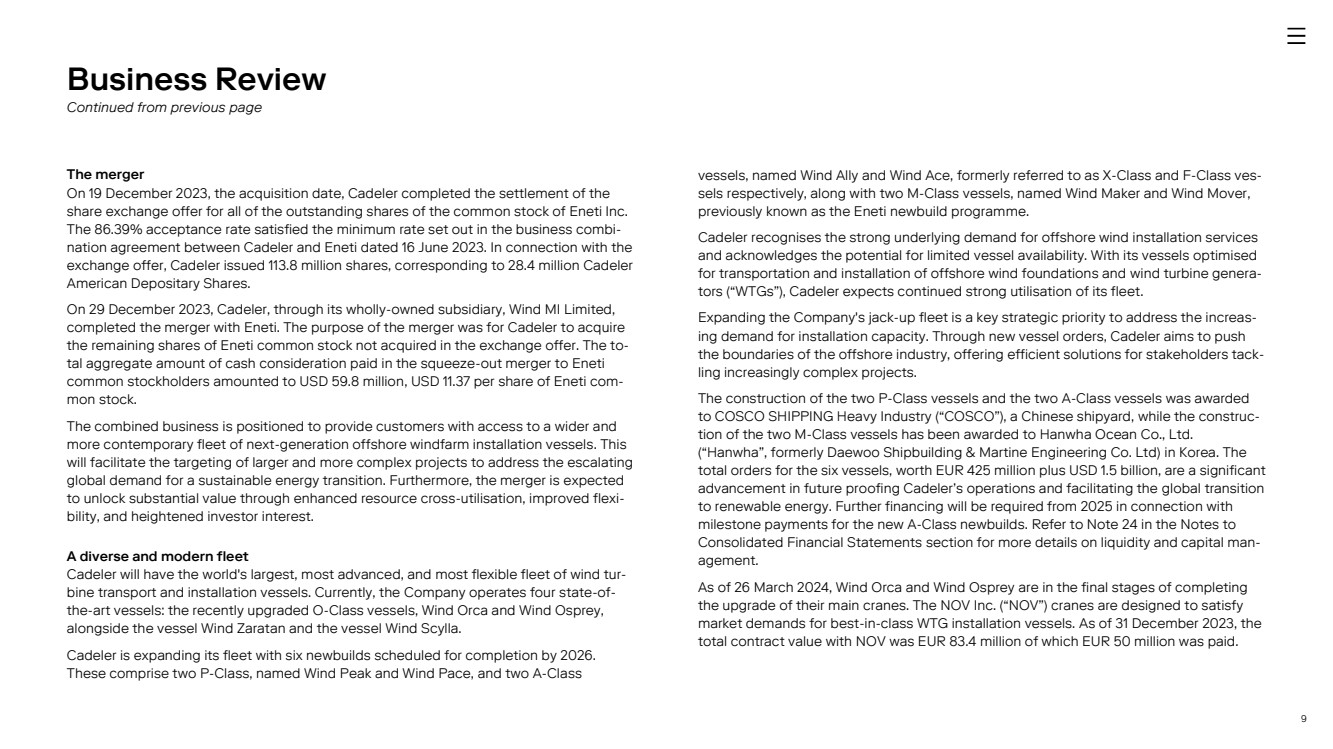

9 The merger On 19 December 2023, the acquisition date, Cadeler completed the settlement of the share exchange offer for all of the outstanding shares of the common stock of Eneti Inc. The 86.39% acceptance rate satisfied the minimum rate set out in the business combi-nation agreement between Cadeler and Eneti dated 16 June 2023. In connection with the exchange offer, Cadeler issued 113.8 million shares, corresponding to 28.4 million Cadeler American Depositary Shares. On 29 December 2023, Cadeler, through its wholly-owned subsidiary, Wind MI Limited, completed the merger with Eneti. The purpose of the merger was for Cadeler to acquire the remaining shares of Eneti common stock not acquired in the exchange offer. The to-tal aggregate amount of cash consideration paid in the squeeze-out merger to Eneti common stockholders amounted to USD 59.8 million, USD 11.37 per share of Eneti com-mon stock. The combined business is positioned to provide customers with access to a wider and more contemporary fleet of next-generation offshore windfarm installation vessels. This will facilitate the targeting of larger and more complex projects to address the escalating global demand for a sustainable energy transition. Furthermore, the merger is expected to unlock substantial value through enhanced resource cross-utilisation, improved flexi-bility, and heightened investor interest. A diverse and modern fleet Cadeler will have the world's largest, most advanced, and most flexible fleet of wind tur-bine transport and installation vessels. Currently, the Company operates four state-of-the-art vessels: the recently upgraded O-Class vessels, Wind Orca and Wind Osprey, alongside the vessel Wind Zaratan and the vessel Wind Scylla. Cadeler is expanding its fleet with six newbuilds scheduled for completion by 2026. These comprise two P-Class, named Wind Peak and Wind Pace, and two A-Class vessels, named Wind Ally and Wind Ace, formerly referred to as X-Class and F-Class ves-sels respectively, along with two M-Class vessels, named Wind Maker and Wind Mover, previously known as the Eneti newbuild programme. Cadeler recognises the strong underlying demand for offshore wind installation services and acknowledges the potential for limited vessel availability. With its vessels optimised for transportation and installation of offshore wind foundations and wind turbine genera-tors (“WTGs”), Cadeler expects continued strong utilisation of its fleet. Expanding the Company's jack-up fleet is a key strategic priority to address the increas-ing demand for installation capacity. Through new vessel orders, Cadeler aims to push the boundaries of the offshore industry, offering efficient solutions for stakeholders tack-ling increasingly complex projects. The construction of the two P-Class vessels and the two A-Class vessels was awarded to COSCO SHIPPING Heavy Industry (“COSCO”), a Chinese shipyard, while the construc-tion of the two M-Class vessels has been awarded to Hanwha Ocean Co., Ltd. (“Hanwha”, formerly Daewoo Shipbuilding & Martine Engineering Co. Ltd) in Korea. The total orders for the six vessels, worth EUR 425 million plus USD 1.5 billion, are a significant advancement in future proofing Cadeler’s operations and facilitating the global transition to renewable energy. Further financing will be required from 2025 in connection with milestone payments for the new A-Class newbuilds. Refer to Note 24 in the Notes to Consolidated Financial Statements section for more details on liquidity and capital man-agement. As of 26 March 2024, Wind Orca and Wind Osprey are in the final stages of completing the upgrade of their main cranes. The NOV Inc. (“NOV”) cranes are designed to satisfy market demands for best-in-class WTG installation vessels. As of 31 December 2023, the total contract value with NOV was EUR 83.4 million of which EUR 50 million was paid. Business Review Continued from previous page |

|

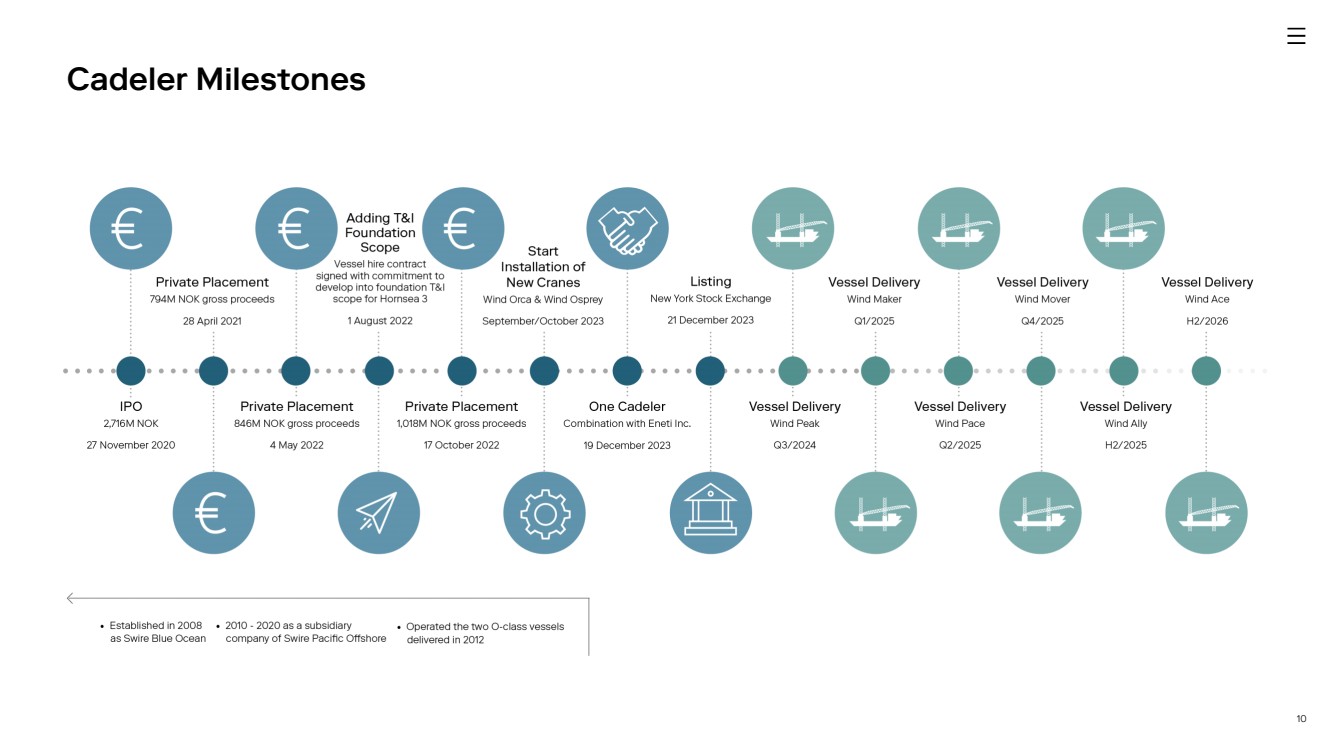

10 Cadeler Milestones |

|

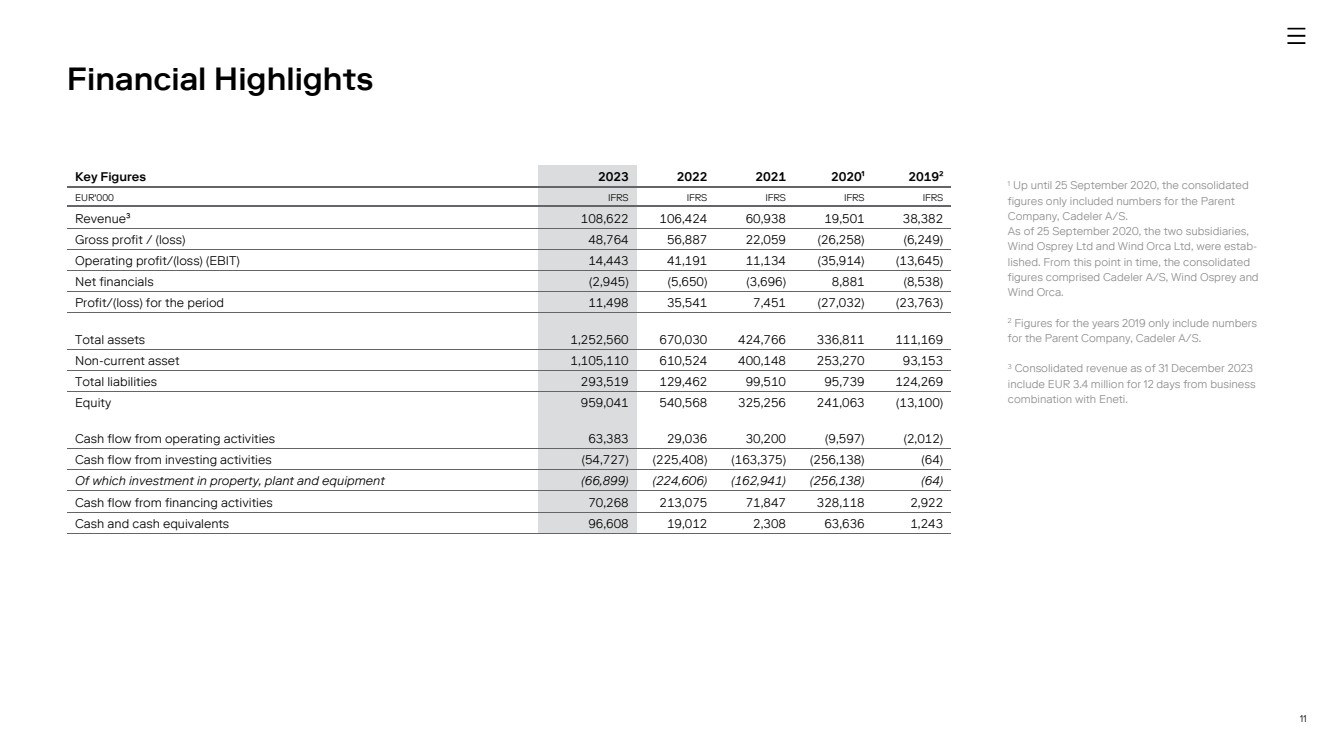

11 Financial Highlights 1 Up until 25 September 2020, the consolidated figures only included numbers for the Parent Company, Cadeler A/S. As of 25 September 2020, the two subsidiaries, Wind Osprey Ltd and Wind Orca Ltd, were estab-lished. From this point in time, the consolidated figures comprised Cadeler A/S, Wind Osprey and Wind Orca. 2 Figures for the years 2019 only include numbers for the Parent Company, Cadeler A/S. 3 Consolidated revenue as of 31 December 2023 include EUR 3.4 million for 12 days from business combination with Eneti. Key Figures 2023 2022 2021 2020¹ 2019² EUR'000 IFRS IFRS IFRS IFRS IFRS Revenue³ 108,622 106,424 60,938 19,501 38,382 Gross profit / (loss) 48,764 56,887 22,059 (26,258) (6,249) Operating profit/(loss) (EBIT) 14,443 41,191 11,134 (35,914) (13,645) Net financials (2,945) (5,650) (3,696) 8,881 (8,538) Profit/(loss) for the period 11,498 35,541 7,451 (27,032) (23,763) Total assets 1,252,560 670,030 424,766 336,811 111,169 Non-current asset 1,105,110 610,524 400,148 253,270 93,153 Total liabilities 293,519 129,462 99,510 95,739 124,269 Equity 959,041 540,568 325,256 241,063 (13,100) Cash flow from operating activities 63,383 29,036 30,200 (9,597) (2,012) Cash flow from investing activities (54,727) (225,408) (163,375) (256,138) (64) Of which investment in property, plant and equipment (66,899) (224,606) (162,941) (256,138) (64) Cash flow from financing activities 70,268 213,075 71,847 328,118 2,922 Cash and cash equivalents 96,608 19,012 2,308 63,636 1,243 |

|

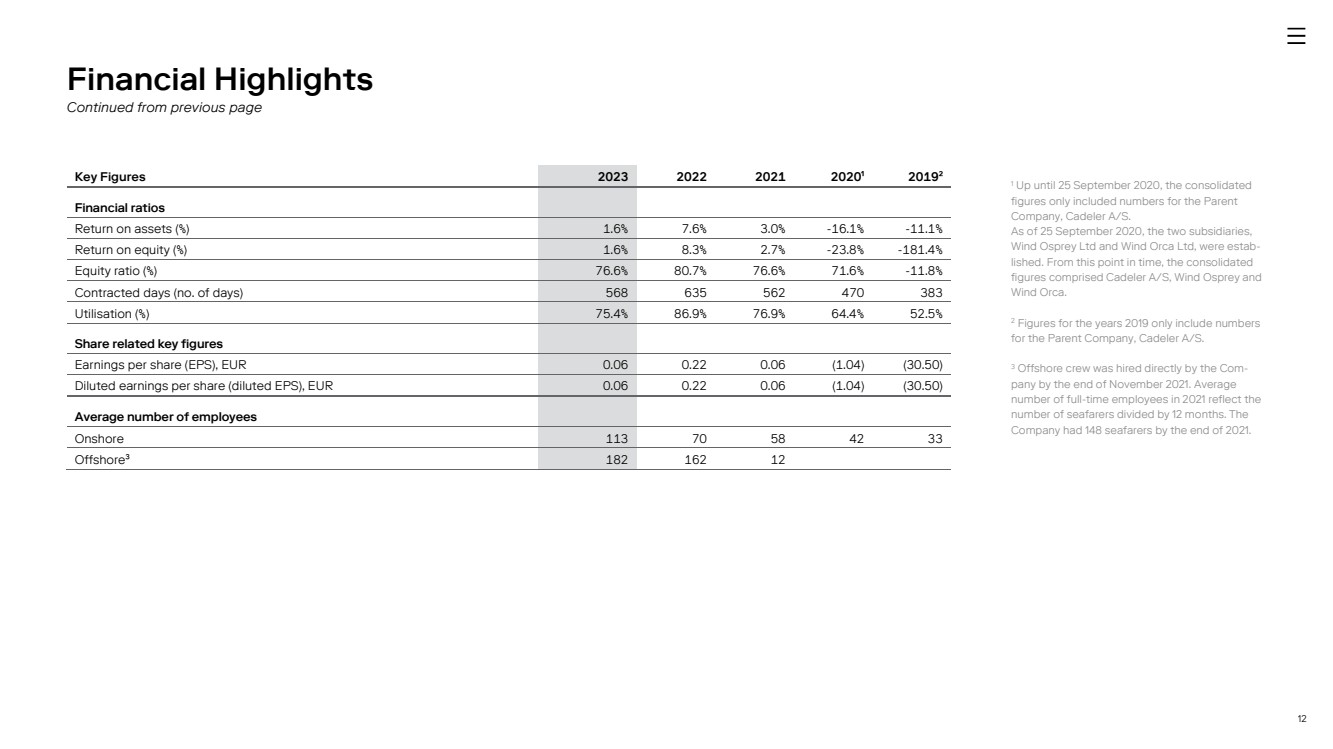

12 Key Figures 2023 2022 2021 2020¹ 2019² Financial ratios Return on assets (%) 1.6% 7.6% 3.0% -16.1% -11.1% Return on equity (%) 1.6% 8.3% 2.7% -23.8% -181.4% Equity ratio (%) 76.6% 80.7% 76.6% 71.6% -11.8% Contracted days (no. of days) 568 635 562 470 383 Utilisation (%) 75.4% 86.9% 76.9% 64.4% 52.5% Share related key figures Earnings per share (EPS), EUR 0.06 0.22 0.06 (1.04) (30.50) Diluted earnings per share (diluted EPS), EUR 0.06 0.22 0.06 (1.04) (30.50) Average number of employees Onshore 113 70 58 42 33 Offshore³ 182 162 12 Financial Highlights Continued from previous page 1 Up until 25 September 2020, the consolidated figures only included numbers for the Parent Company, Cadeler A/S. As of 25 September 2020, the two subsidiaries, Wind Osprey Ltd and Wind Orca Ltd, were estab-lished. From this point in time, the consolidated figures comprised Cadeler A/S, Wind Osprey and Wind Orca. 2 Figures for the years 2019 only include numbers for the Parent Company, Cadeler A/S. 3 Offshore crew was hired directly by the Com-pany by the end of November 2021. Average number of full-time employees in 2021 reflect the number of seafarers divided by 12 months. The Company had 148 seafarers by the end of 2021. |

|

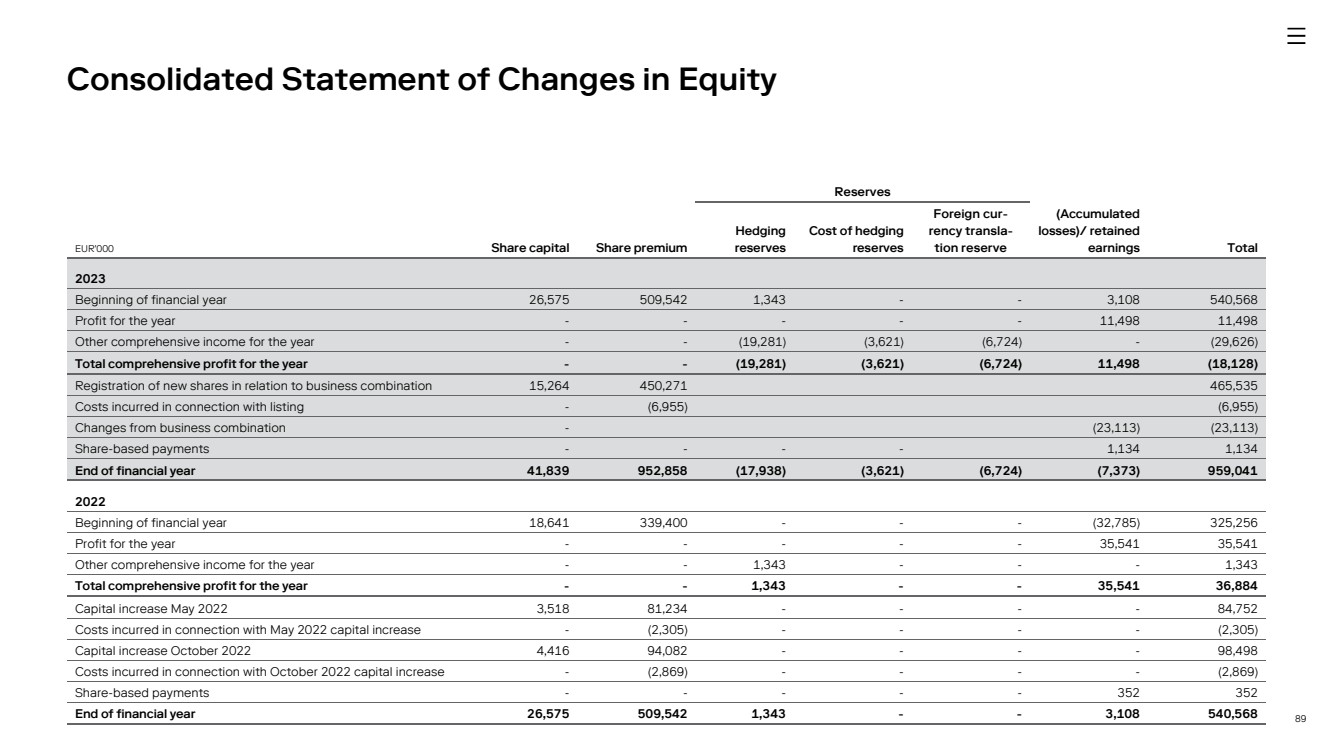

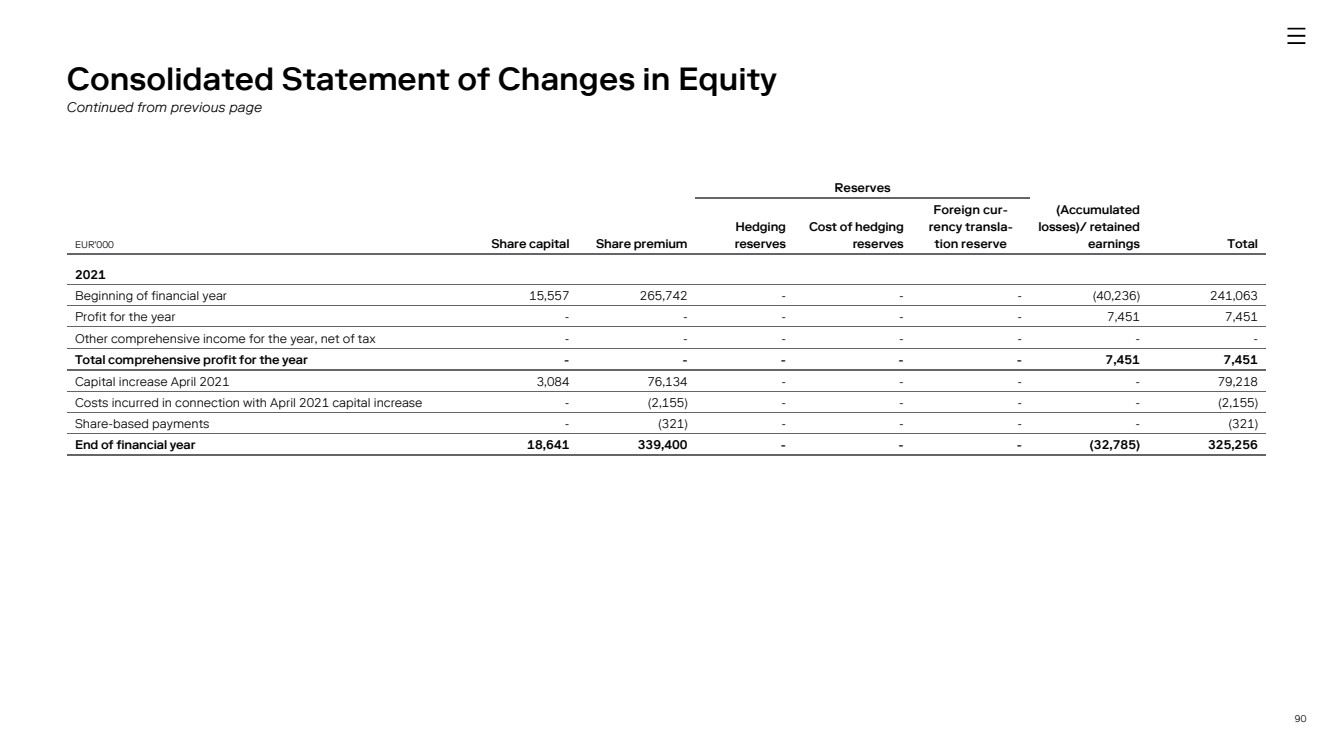

13 Capital structure and funding Equity On 31 December 2023, equity amounted to EUR 959 million (EUR 541 million in 2022 and EUR 325 million in 2021), as a result of profit for the year of EUR 11 million (EUR 36 million in 2022 and EUR 7 million in 2021), EUR 30 million loss value adjustment of hedges (EUR 1.3 million gain in 2022) and net capital increase of EUR 459 million (EUR 178 million in 2022 and EUR 77 million in 2021). In 2022, the Company conducted two successful private placements. The first, which took place in May, saw the issuance of 26.2 million shares at a price of NOK 32.32 per share, while the second in October placed 32.9 million shares at a price of NOK 31.00 per share. Overall, the Company raised approximately EUR 183 million before transaction costs. As of 31 December 2022, the Company had 197.6 million shares in issue, compared to 138.6 million shares at the beginning of the reporting period. The Fleet As of 31 December 2023, the Cadeler Group’s fleet consists of four operating vessels, Wind Orca, Wind Osprey, Wind Scylla and Wind Zaratan. In addition, the Cadeler Group has orders for two P-Class, two A-Class and two M-Class vessels, the Cadeler newbuild programme. The Operating Vessels The Cadeler Group’s two operating O-Class vessels are considered by the Cadeler Group to be well suited for windfarm installation, maintenance and decommissioning. The oper-ating O-Class vessels feature a six-leg design, which allows them to operate even on sites with challenging seabed conditions. Their cargo area and high-capacity deck load-ing offer considerable flexibility in the T&I of WTGs and foundations. In December 2020, the Cadeler Group signed a contract to replace the main crane of Wind Orca and subsequently, in June 2021, the Cadeler Group executed an option to re-place the main crane of Wind Osprey. The crane upgrades for the two operating O-Class vessels started in September 2023 and, as of 26 March 2024, are nearing completion. The total cost of upgrading the cranes on Wind Orca and Wind Osprey is expected to reach up to EUR 120 million, of which EUR 61 million had been paid as of 31 December 2023. The remaining payments are due in 2024. On 19 December 2023, as a result of the business combination with Eneti, the Cadeler Group acquired two operating vessels, Wind Scylla and Wind Zaratan. Sailing at speeds of 12 knots or over, Wind Scylla is outfitted with 105-metre-long legs that can install components in water depths of up to 65 metres. Wind Scylla makes Cadeler's fleet unparalleled in the offshore wind sector for the installation and mainte-nance of wind farms. Wind Scylla has a useable deck space in excess of 5,000 m2 and is fitted with a 1,540 metric tons leg crane, making it ideal for deep water and large wind farm components. After meeting stringent Japanese flag requirements, Wind Zaratan sails under the Japa-nese flag. The growing offshore wind market in Japan coupled with a lack of jack-up ves-sels operating under Japanese flag (a requirement for offshore wind contractors when working in Japanese territorial waters) places Wind Zaratan in a strong position for win-ning future contracts. Finance Review |

|

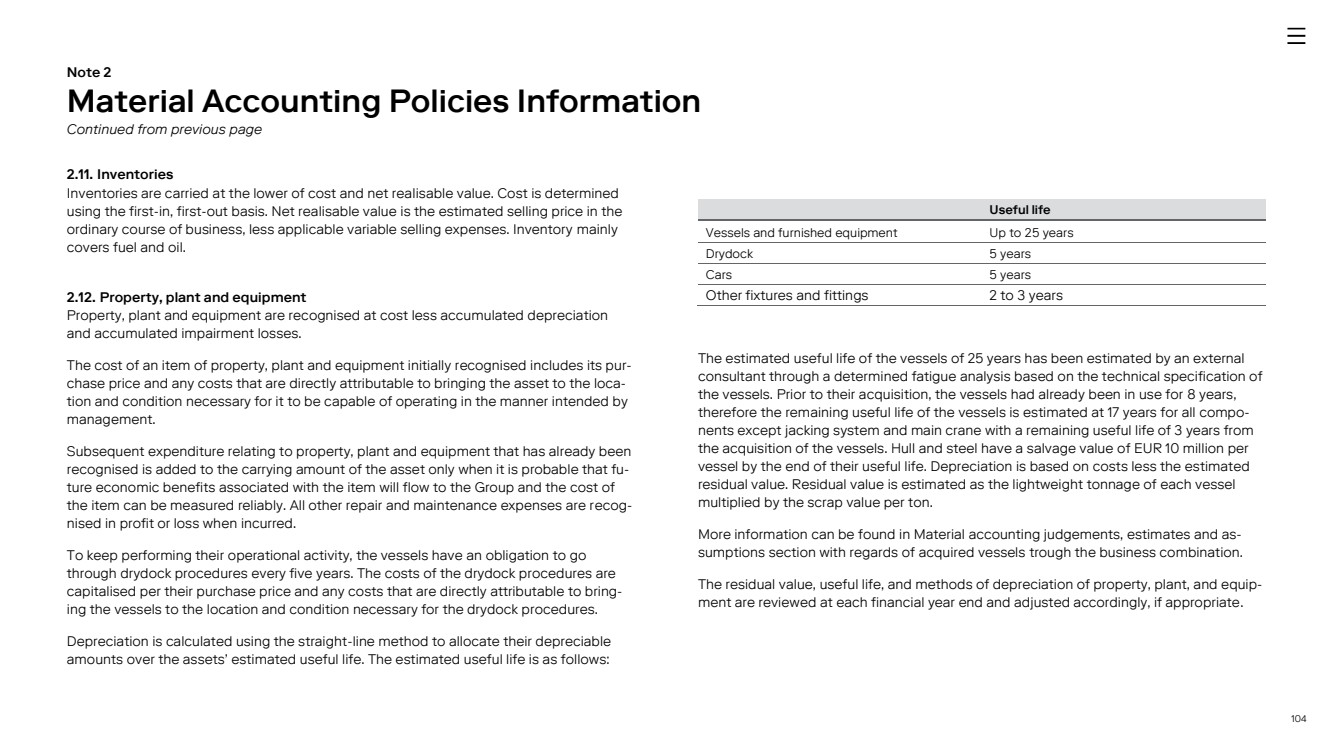

14 Below is a detailed overview of the current specifications of the Cadeler Group’s four op-erating vessels, Wind Orca, Wind Osprey, Wind Scylla and Wind Zaratan: The newbuilds (currently under construction) In June 2021, the Cadeler Group entered into contracts with COSCO regarding the build-ing of two new WTG installation P-Class newbuild vessels. The two P-Class newbuilds are expected to be delivered in the third quarter of 2024 and the second quarter of 2025, respectively. On 7 September 2023, Cadeler incorporated two new subsidiaries, WIND N1064 Limited and WIND N1063 Limited, which are registered and domiciled in Cyprus for the purpose of acquiring the P-Class newbuilds. The P-Class newbuilds are designed to operate at difficult sites and with what the Cadeler Group believes to be some of the most advanced equipment in the industry. The P-Class newbuilds will be able to transport and install seven complete 15 megawatt tur-bine sets per load or five 20+ megawatt turbines, thereby cutting down the number of trips needed for each project and thus accelerating the installation speed. The Cadeler Group currently expects that the P-Class newbuilds will have industry leading lifting height and payload capabilities. With the two P-Class newbuilds, the Cadeler Group be-lieves it will be able to stay at the forefront of the industry. Moreover, the Cadeler Group has focused on the sustainability and CO2-footprint of the two P-Class newbuilds as part of the design phase to ensure a more sustainable operation of the new P-Class new-builds. The first of the two P-Class newbuilds has already been contracted for the Sofia Project for the transport and installation of 100 14 megawatt WTGs, while the second P-Class newbuild is expected to be first utilised for the East Anglia Three Project consisting of installation of 95 WTGs. The total contract value for the construction of the P-Class newbuilds is approximately EUR 572 million, of which EUR 137 million and EUR 14 million was paid in 2021 and 2023 respectively. The remaining scheduled payments are due between 2024 and 2025. Of the total contract value, USD 390 million will be paid in USD and EUR 220 million will be paid in EUR. The first milestone payment for the P-Class newbuilds was financed in part by the proceeds of Cadeler’s initial public offering in November 2020 and a private placement in April 2021. The remaining payments for the two P-Class newbuilds are ex-pected to be financed through debt. Finance Review Continued from previous page 1 Crane upgrades, expected to be completed early Q2/2024, will add capabilities to install next generation 20+MW turbines 2 Post crane upgrade Name Wind Zaratan Wind Scylla Wind Orca Wind Osprey Type Turbine (WTIV) Turbine (WTIV) Turbine (WTIV) Turbine (WTIV) Class (Cadeler definition) Z-Class S-Class O-Class O-Class Built / expected delivery (quarter / year) 2012 2015 2012 / Q1/2024¹ 2012 / Q1/2024¹ Main crane capacity (tonnes) 800 1540 1600² 1600² Hook Height (meters) 92 105 160 160 Turbine installation capacity (MW) 9.5 12-14 15-20 15-20 |

|

15 Cadeler Group has also placed orders with COSCO for the construction of two A-Class newbuilds. In May 2022, the Cadeler Group signed a contract with COSCO regarding the building of one A-Class newbuild WTIV expected to be delivered in the fourth quarter of 2025. The contract included an option for one additional P-Class or A-Class vessel. The Cadeler Group has experienced strong employment prospects for the A-Class newbuild, which was evidenced by the Cadeler Group’s contract with Ørsted A/S (“Ørsted”) for foundation installation at Hornsea 3 offshore wind farm, which is set to utilise one A-Class newbuild. As a result, in November 2022, the Cadeler Group exercised the option to order one additional A-Class newbuild, which is expected to be delivered in the sec-ond half of 2026. This A-Class newbuild will upon delivery be the second purpose-built wind foundation installation vessel in the Cadeler Group’s fleet. In connection with the exercise of the option, and entering into a definitive contract, the Cadeler Group has en-tered into a letter of intent regarding the construction of an additional A-Class newbuild vessel. The A-Class newbuilds are based on the P-Class specifications and will be hybrid vessels for T&I of both foundations and WTGs. The A-Class newbuilds will be able to transport up to six XL monopile foundations per round trip and, if needed, may within a short period of time be converted from being a foundation installation vessel to a WTG installation ves-sel. The A-Class newbuilds will, as the P-Class newbuilds, be able to transport and install seven complete 15 megawatt turbine sets per load or five 20+ megawatt turbines, thereby cutting down the number of trips needed for each project and thus accelerating the installation speed. The Cadeler Group believes the large transport capacity will in-crease operational efficiency substantially. The total value of the contracts for the A-Class newbuilds is approximately EUR 657 mil-lion. After down payments of an aggregate EUR 167 million in June 2022 and December 2022, financed through private placements completed in May and October 2022, respec-tively, the remaining amounts are due in 2025 and 2026. Of the total contract value, USD 495 million will be paid in USD and EUR 205 million will be paid in EUR. The remaining payments on the A-Class newbuilds are currently expected to be financed through se-cured senior debt and cash flow from the operations. On 19 December 2023, as a result of the Business Combination with Eneti, the Cadeler Group added two M-Class vessels to its newbuild vessels, for the construction of which there are two contracts in place with Hanwha. The M-Class newbuilds, Wind Maker (formerly known as “Nessie”) and Wind Mover (for-merly known as “Siren”), will operate with an impressive high capacity 2,600 metric tons main crane which will revolve around the starboard aft leg, allowing the safe installation and maintenance of heavy foundations and the components relating to offshore wind turbines. Both vessels have been designed to operate in water depths of up to 65 me-tres and at significant wave heights of 2 metres whilst the vessel itself will be above sea level installing and maintaining offshore structures. Finance Review Continued from previous page |

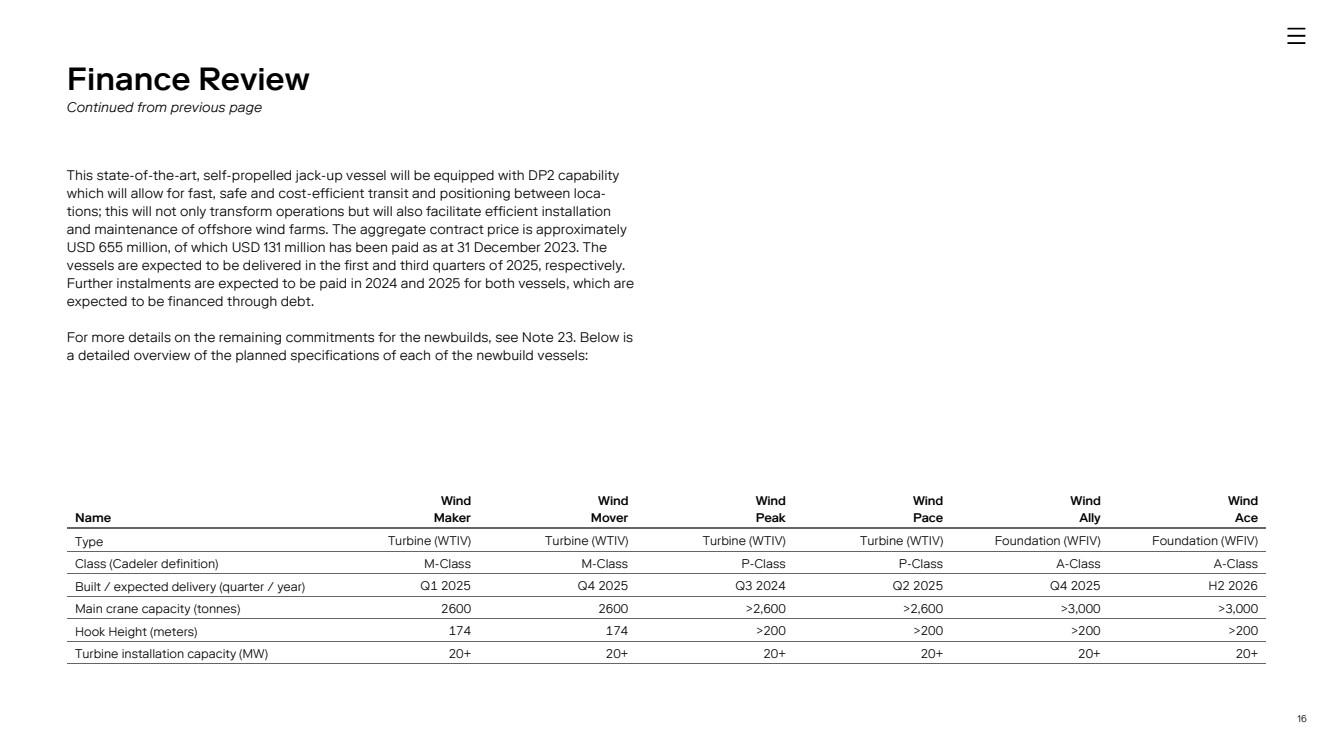

|

16 This state-of-the-art, self-propelled jack-up vessel will be equipped with DP2 capability which will allow for fast, safe and cost-efficient transit and positioning between loca-tions; this will not only transform operations but will also facilitate efficient installation and maintenance of offshore wind farms. The aggregate contract price is approximately USD 655 million, of which USD 131 million has been paid as at 31 December 2023. The vessels are expected to be delivered in the first and third quarters of 2025, respectively. Further instalments are expected to be paid in 2024 and 2025 for both vessels, which are expected to be financed through debt. For more details on the remaining commitments for the newbuilds, see Note 23. Below is a detailed overview of the planned specifications of each of the newbuild vessels: Finance Review Continued from previous page Name Wind Maker Wind Mover Wind Peak Wind Pace Wind Ally Wind Ace Type Turbine (WTIV) Turbine (WTIV) Turbine (WTIV) Turbine (WTIV) Foundation (WFIV) Foundation (WFIV) Class (Cadeler definition) M-Class M-Class P-Class P-Class A-Class A-Class Built / expected delivery (quarter / year) Q1 2025 Q4 2025 Q3 2024 Q2 2025 Q4 2025 H2 2026 Main crane capacity (tonnes) 2600 2600 >2,600 >2,600 >3,000 >3,000 Hook Height (meters) 174 174 >200 >200 >200 >200 Turbine installation capacity (MW) 20+ 20+ 20+ 20+ 20+ 20+ |

|

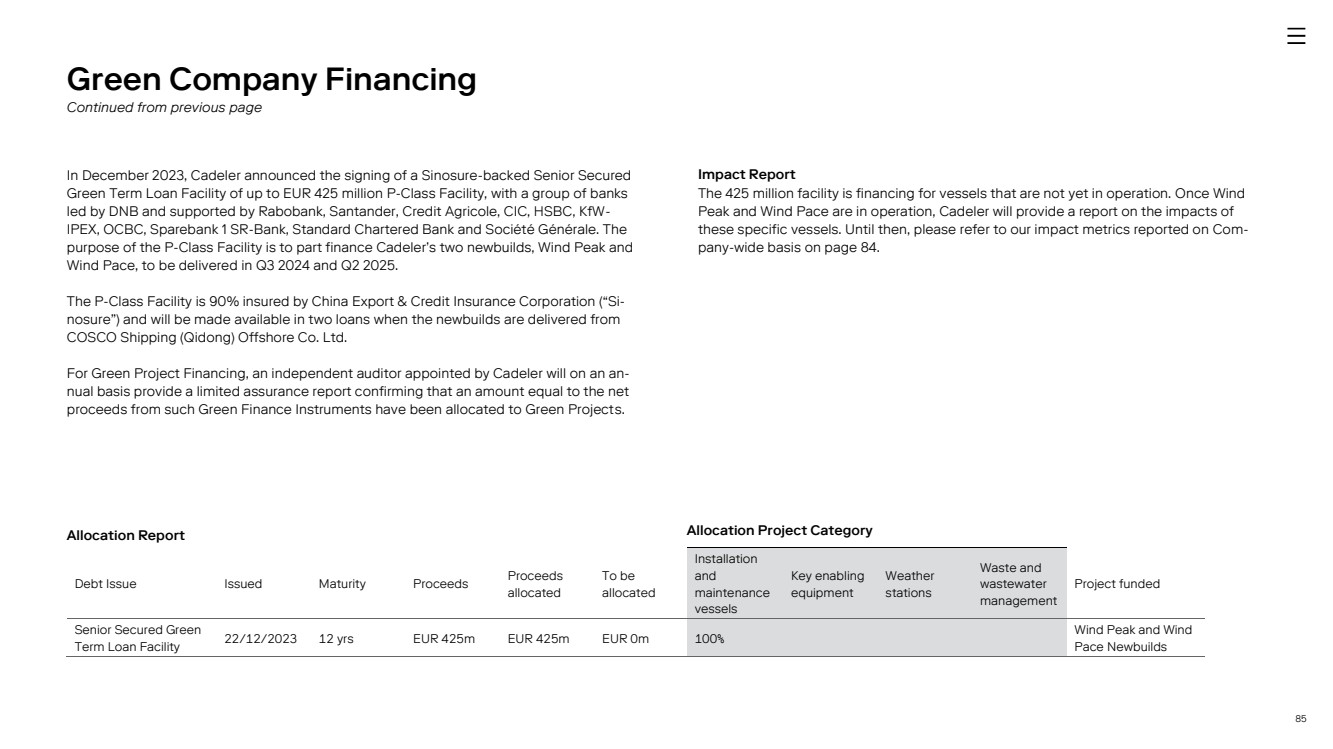

17 Funding On 29 June 2022, the Cadeler Group entered into a senior secured green revolving credit facility (the “Debt Facility”), which provided for a three-year revolving credit facility of up to EUR 185 million. The Debt Facility was entered into for the purpose of refinancing ex-isting facility agreements, obtaining financing for general corporate purposes and work-ing capital requirements. On 16 June 2023, Cadeler amended its Debt Facility, increasing the guarantee facility to EUR 60 million and the committed revolving credit facility to EUR 250 million, resulting in a total Debt Facility of EUR 310 million. Additionally, an accordion option allows for a po-tential EUR 100 million increase by adding a term loan facility, subject to lender discre-tion and export credit agency guarantee. On 7 December 2023, Cadeler secured a new senior secured credit and guarantee facility (the “New Debt Facility”) of up to EUR 550 million with DNB Bank ASA, Rabobank, Credit Agricole, Danske Bank, OCBC, Standard Chartered Bank, and Société Générale. This fa-cility includes various tranches: a revolving credit facility of EUR 250 million (5-year tenor), a revolving credit facility of EUR 100 million (18-month tenor), a term loan of EUR 100 million (8.5-year tenor) guaranteed by the Danish export and Investment Fund of Denmark (EIFO), and an uncommitted guarantee facility of EUR 100 million. On 15 November 2023, Cadeler entered an unsecured term loan facility of EUR 50 million with HSBC, (the “Holdco Facility”), supporting wind installation activities and general cor-porate purposes. This facility includes an accordion option of up to EUR 50 million and contains change of control provisions. On 22 December 2023, Cadeler and its subsidiaries secured a Sinosure-backed green term loan facility of up to EUR 425 million, (the “P-Class Facility”), to finance P-Class newbuilds. This facility includes various securities and change of control provisions. In connection with the Business Combination, the Group acquired a senior secured green term loan facility, which Eneti entered into in November 2023, of up to USD 436 million (the “New Credit Facility”) with a group of international banks and export credit agencies co-arranged and co-underwritten by Crédit Agricole Corporate and Investment Bank and Société Générale, and with Société Générale as Green Loan Coordinator. The New Credit Facility finances approximately 65% of the purchase cost of the M-Class newbuilds. Additional financing of approximately EUR 450 million will be required from 2025 for A-Class newbuilds milestone payments. The Group entered into interest rate swap con-tracts with the Group’s main bank and related these to the RCF and the future loans. The interest rate risk arising from the loans have been partially swapped from 3M EURIBOR to a fixed rate. The average fixed rate of the swaps is 2.8%. Income statement Revenue In 2023, the Company saw a modest revenue growth of 2%, amounting to EUR 109 mil-lion. Despite a lower utilisation rate of 75% due to upgrades on Wind Orca and Wind Os-prey in Q4 2023, the revenue growth is commendable. Additional revenue streams in-cluded EUR 3.4 million from the business combination with Eneti and a further EUR 5 mil-lion from the cancellation of the Aflandshage contract. Costs Cost of sales for 2023 rose by 20% to EUR 60 million, up from EUR 50 million the previ-ous year. This increase was largely due to the impairment of the sold main crane for Wind Orca, costing EUR 5 million. Other contributing factors include an additional EUR 3.8 mil-lion from the business combination with Eneti. Finance Review Continued from previous page |

|

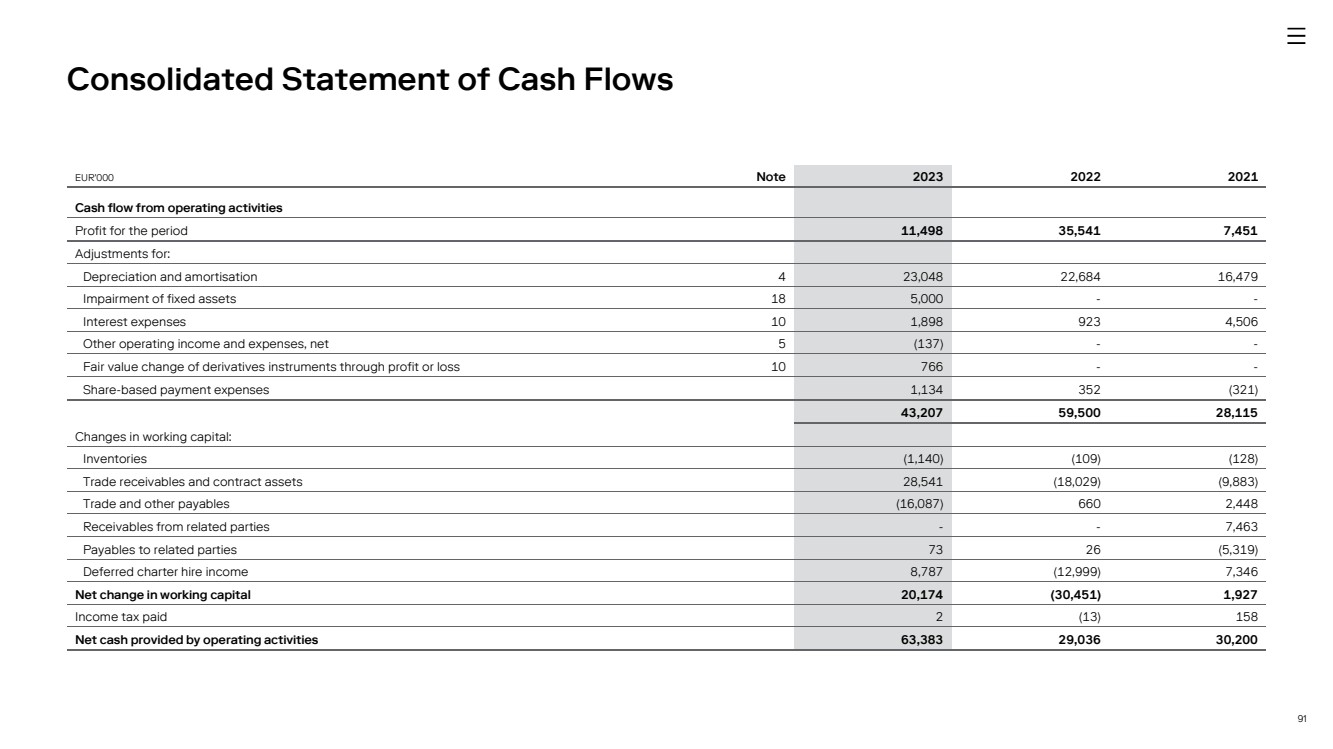

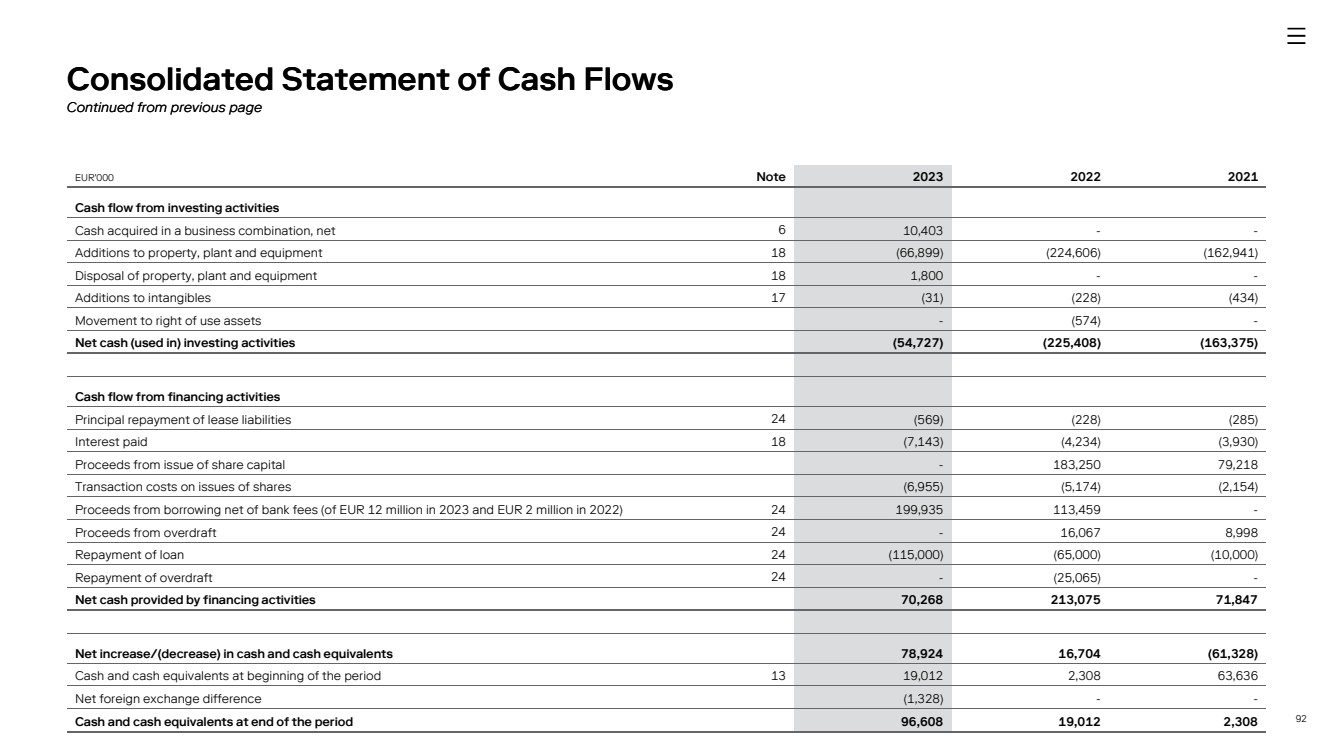

18 Administrative expenses saw a significant increase from EUR 16 million to EUR 34 million. This was primarily due to transaction costs from the business combination amounting to EUR 7.7 million and an increase in employee compensation due to a rise in onshore em-ployees from 70 in 2022 to 113 in 2023, adding approximately EUR 9 million in costs. EBITDA and Adjusted EBITDA The Company projected an EBITDA range of EUR 40 million to EUR 45 million on 13 No-vember 2023. The actual EBITDA for the year was EUR 42 million, down from EUR 64 mil-lion in 2022 due to higher cost of sales and administrative expenses. The Company also provided a revised outlook for the adjusted EBITDA in the range of EUR 47 million to EUR 52 million, with the actual Adjusted EBITDA for the year coming in at EUR 50 million. For further information please refer to Alternative Performance Measures section. Financial Income and Expenses Finance income decreased EUR 2 million from EUR 4 million in 2022 to EUR 2 million in 2023, mainly driven by EUR 3 million decrease in foreign exchange gains and an increase of EUR 1 million in interests gained. Finance costs decreased from EUR 10 million in 2022 to EUR 4 million in 2023, due to EUR 7 million decrease in foreign exchange losses and an increase of EUR 1 million increase in interests linked to debt institutions. Profit for the year The Group’s net result for the year was a profit of EUR 11 million, which decreased from EUR 36 million in 2022, mainly driven by changes in cost of sales and administrative ex-penses. Cadeler A/S, the Parent Company, reported a net profit of EUR 11 million, down from EUR 27 million in 2022. This result is similar to group with minor differences at-tributed to the treatment of the two subsidiaries, Wind Orca Ltd and Wind Osprey Ltd, which are measured at cost in the Parent Company. Cash flows Net cash from operating activities in 2023 was EUR 63 million, double that of 2022. The increase was primarily driven by a positive net change in working capital and adjustments such as impairment of fixed assets. Net cash used in investing activities in 2023 was EUR 55 million, down from EUR 225 million in 2022, due to the absence of large asset invest-ments. In 2023, the business combination with Eneti was completed via a share ex-change and EUR 10 million net cash. Net cash from financing activities decreased by EUR 143 million to EUR 70 million in 2023, due to proceeds from issue of shares impact-ing 2022 and partially offset by the Holdco Facility for EUR 50 million from HSBC in 2023. The Company had significant headroom to comply with its debt covenants and on 31 De-cember 2023, the Company had available liquidity of EUR 435 million from cash at hand and available committed facilities like the New Debt facility and the Holdco Facility. Assets As of 31 December 2023, the Company's total assets amounted to EUR 1,253 million, a significant increase from EUR 670 million in 2022. This increase can be attributed to the business combination. Other additions to property, plant, and equipment are described in Note 18. Property, Plant and Equipment The Cadeler Group’s property, plant, and equipment increased to EUR 1.1 billion in 2023, up from EUR 606 million in 2022. This primarily comprised the operating vessels Wind Scylla and Wind Zaratan, the newbuilds under construction and the M-Class down pay-ments for EUR 144 million. The Cadeler Group does not own any substantial real estate. The Cadeler Group is leasing its current headquarters in Copenhagen, Denmark. The Cadeler Group entered into an agreement with Castellum Denmark regarding the lease for new headquarters in Copenhagen, Denmark, with effect from February 2024. Finance Review Continued from previous page |

|

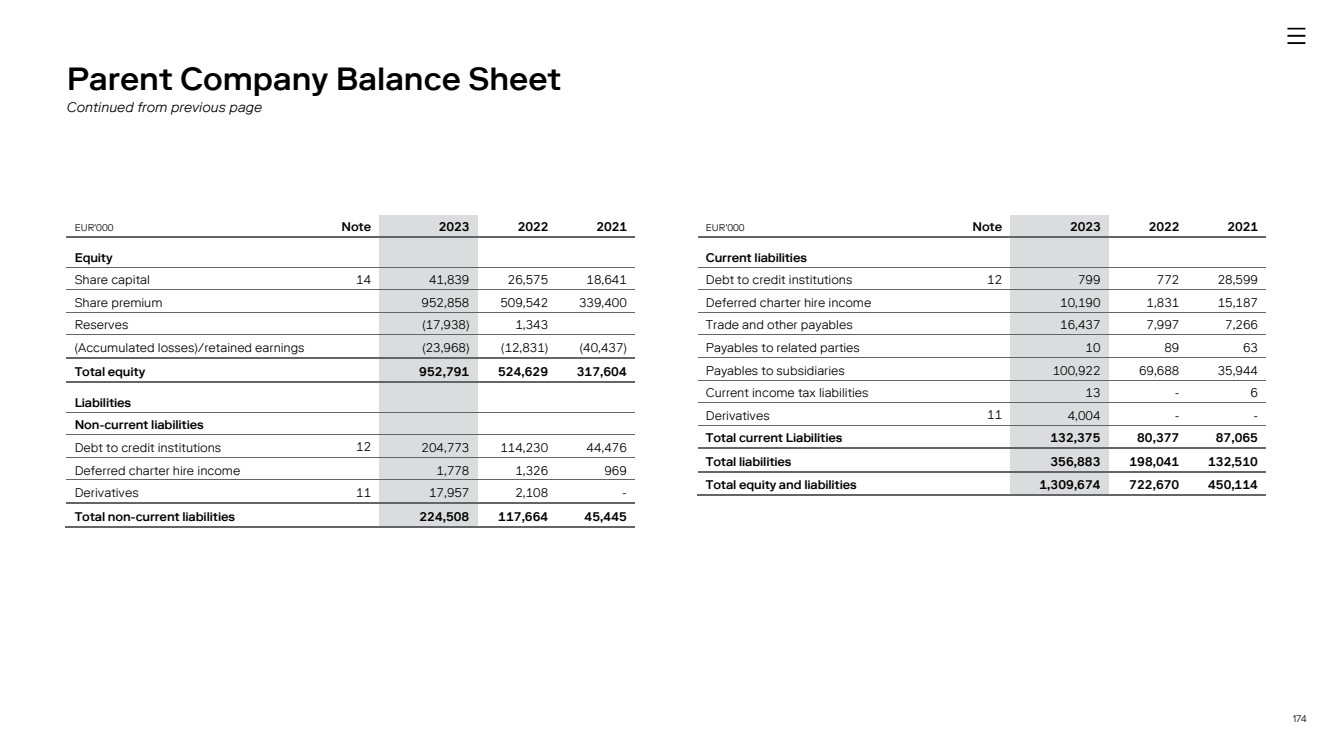

19 Parent Company The activities of the Parent Company are similar to the activities described for the Group. The finance review as described for the Group is also applicable for the Parent Company, except for the material differences described below. The Parent Company’s revenue is EUR 109 million (EUR 108 million in 2022). Total expenses for the Parent Company in 2023 amount to EUR 91 million (EUR 76 million in 2022) compared to EUR 94 million (EUR 65 million in 2022) for the Group. As the ves-sels of the Group are owned by subsidiaries of the Parent Company, no vessel deprecia-tion or vessel insurance is recognised in the Parent Company. Instead, the Parent Com-pany is subject to bareboat charges from vessel owning subsidiaries. This amounts to EUR 30 million in 2023 (EUR 34 million in 2022). Total assets were EUR 1.3 billion (EUR 723 million in 2022), which is the same as the Group EUR 1.3 billion (670 million 2022). The increase in the parent company is due to the addition to investments in subsidiaries from the business combination with Eneti for EUR 496 million. Total liabilities were EUR 357 million (EUR 198 million in 2022), the difference to the Group EUR 334 million (EUR 129 million in 2022) being driven by an increase of EUR 30 million in payables to subsidiaries. Equity amounted to EUR 953 million (EUR 525 million in 2022), compared to the Group EUR 959 million (EUR 541 million in 2022). Knowledge resources The Company is committed to attracting and retaining highly skilled professionals to meet the needs of its customers and provide exceptional service. This includes recruit-ing experienced engineers who can modify the Company's vessels to meet the specific requirements of customer projects, as well as commercial experts with relevant industry knowledge. The Company's ongoing investment in talent enables it to maintain a com-petitive edge in the market and position itself for long-term success. Research and development activities The Company's Research and Development department is focused on enhancing the fleet and exploring innovative solutions to optimise operations within the offshore wind market. By continuing to invest in R&D, the Company aims to maintain its competitive edge, achieve greater operational efficiency, and meet the evolving needs of its customers. The Company recognises the importance of ongoing research and development activi-ties in ensuring its continued growth and success in the years ahead. Special risks Operational risks The Company is vulnerable to a loss of revenue if any of its vessels are taken out of op-eration or if the delivery of newbuilds is delayed. The Company's fleet currently consists of four windfarm installation vessels, Wind Orca, Wind Osprey, Wind Scylla and Wind Zaratan. The Company also has orders for six newbuilds, four WTIVs, the P-Class and the M-Class newbuilds, and two wind foundation installation vessels, the A-Class newbuilds, and has entered into a letter of intent for the delivery of a third A-class newbuild. Finance Review Continued from previous page |

|

20 If any of the vessels in the Company's operational fleet at any given time are taken out of operation or delivered later than anticipated, due to risks such as delays in the delivery of the newbuilds or operational incidents, this could materially impact the Company's busi-ness, prospects, financial results, and condition. The Company has contracted with COSCO to take delivery of four newbuild vessels in total in the period from the third quarter of 2024 to the second half of 2026. At the same time, the Company has a contract with Hanwha to take delivery of two newbuild vessels in 2025 and has entered into a letter of intent with COSCO for the construction of an ad-ditional A-Class newbuild. Any problems that may affect China or Korea in general, the general availability of components or material needed, or the shipyard specifically could lead to delays of one or all six newbuild vessels. The vessels may also be subject to up-grades, refurbishments, and/or repairs, which are subject to risks, including delays and cost overruns, which could have an adverse impact on the Company's available cash re-sources, results of operations, and its ability to comply with financial covenants pursuant to its financing arrangements. The Group is operating in the offshore industry and is thus subject to inherent hazards, such as breakdowns, technical problems, harsh weather conditions, environmental pollu-tion, force majeure situations (nationwide strikes, etc.), collisions and groundings. These hazards can cause personal injury or loss of life, severe damage to or destruction of property and equipment, pollution or environmental damage, claims by third parties or customers and suspension of operations. Windfarm installation vessels, including the Company’s vessels, will also be subject to hazards inherent in marine operations, either while on-site or during mobilisation, such as but not limited to capsizing, sinking, grounding, collision, damage from severe weather and marine life infestations. Operations may also be suspended because of machinery breakdowns, abnormal operating conditions, failure of subcontractors to perform or sup-ply goods or services or personnel shortages. Employment of vessels is key The Group’s income is dependent on project contracts and vessel charters for the em-ployment of the vessels. Typically, these contracts are concluded several years in ad-vance, giving visibility of future deployment. However, there is a risk that it may be diffi-cult for the Company to obtain future cover for the vessels and utilisation may drop. Consequently, the vessels may need to be deployed on lower-yielding work-scopes or remain idle for periods without any compensation to the Company. There can also be off-hire periods as a consequence of accidents, technical breakdown and non-perfor-mance. The cancellation or postponement of one or more employment contracts can have a material adverse impact on the earnings of the Company. Foreign exchange risks The Company is exposed to foreign currency risks. A significant part of the income is in-voiced in EUR, as are most costs, or in DKK, which is pegged to the EUR. Due to the busi-ness combination parts of the Income will be invoiced in USD. A significant proportion of the Company's commitments for the construction of the newbuild vessels will be paid in USD. The currency exposure arising from the newbuild contracts has been partially swapped to EUR at the Company’s banks at an average USD:EUR rate of 0.9187. Another portion of the exposure has been hedged by entering into zero cost collar contracts, se-curing an average USD:EUR rate of between 0.8695 and 0.9466. Finance Review Continued from previous page |

|

21 Debt facility risks The Company has entered into a debt financing agreement with challenging terms, con-ditions, and covenants that restrict its ability to obtain new financing and operate freely. This agreement contains specific financial covenants, and failure to meet them could re-sult in the mandatory repayment of the Company's New Debt Facility, negatively impact-ing the Company’s financial position. The New Debt Facility also constrains the Group's ability to pay dividends in the future. With four operational vessels, the Group's ability to comply with financial covenants will depend on the market value of these vessels and their ability to generate revenue. Their indebtedness could affect future operations and flexibility, limiting the Group's ability to dispose of assets and compete with others in the industry for strategic opportunities. Liquidity risks The Company manages liquidity risk by having enough cash and credit facilities to meet operational needs and new vessel instalments. Financing will be needed from 2025 for milestone payments on new vessels, and the Company is exploring various funding op-tions, including export credit agencies support and an indicative term sheet for financing acquired vessels. Macroeconomic risks The Company operates in multiple jurisdictions and serves a wide range of customers. The macroeconomic factors include, among other things, the rate of growth in the global economy, political conditions and levels of public/institutional spending within the en-ergy sector, currency and interest rate fluctuations and inflation. Additionally, geopolitical tensions may have an impact on the future prospects of the Group’s markets and may increase risk related to the Group’s operations for example with relation to cyber threats to energy supply. Interest risks The Group entered into interest rate swap contracts with the Group’s main bank and re-lated these to the New Debt Facility and the future loans. The interest rate risk arising from the loans has been partially swapped from 3M EURIBOR to a fixed rate. The aver-age fixed rate of the swaps is 2.8%. Credit risks The Company adopts stringent procedures on extending credit terms to customers and on the monitoring of credit risk. The Company deals only with customers with an appro-priate history and obtains sufficient security where appropriate to mitigate credit risk. Historically, only immaterial credit losses have been experienced. Data ethics As per section 99D of the Danish Financial Statements Act, Cadeler as a listed company is obliged to disclose our policy towards data ethics. Cadeler complies with all relevant laws and legislations concerning privacy, confidentiality and cyber security. Cadeler is committed to handling data responsibly. Whilst we seek to harness the benefits that new technology and data usages bring, we will always respect and uphold the fundamental rights of all our employees and stakeholders. Finance Review Continued from previous page |

|

22 The following principles form the basis for Cadeler’s responsible handling of both per-sonal and non-personal data and support and inform our security and personal data poli-cies and procedures: ▶ Transparency. We aim for transparency in all aspects of how we handle data, includ-ing ensuring individuals know how their data is used and for what purpose. ▶ Respect. We respect the rights of all our employees and those we do business with to make informed data choices and are committed to complying with all applicable legal and privacy requirements. ▶ Security. We seek to protect the confidentiality, integrity and availability of Cadeler’s digital assets and data in compliance with relevant laws and industry-specific stand-ards. At Cadeler, we manage data of various types from different sources. Our strategy for handling such information is to ensure that it is created, maintained, and stored in a safe and secure way. Our governance for handling data applies to all personnel, both in our office and on board our vessels, as well as any third-party contractors engaged on our behalf. For third parties, we take particular care to minimise loss of information and sen-sitive information is only disclosed to authorised persons. Cadeler’s approach to data ethics is subject to annual review and approval by Cadeler’s senior leadership team. Impact on the external environment Sustainability remains a strategic objective for the Company and is key to its ability to create long-term value for its shareholders. It represents an opportunity for innovation, improved efficiency and a foundation for growth. The Company is committed to delivering leadership in matters of environment, health and safety, employment, and cor-porate responsibility across its value chain. The Company pursues the long-term goals of decarbonisation, optimising energy efficiency, and improving circularity of its operations. The Company strives to identify and reduce the negative impact that its business has on the environment, monitor per-formance and identify potential areas for improvement. This is done, inter alia, by: ▶ Improvements to vessel design for the newbuild vessels ▶ Planning further improvements focused at energy efficiency, electrification, and im-plementation of renewable fuels ▶ Maintaining vessel compliance with the International Convention for the Prevention of Pollution from Ships (“MARPOL”) requirements and operating on low sulphur fuels For more information, see our annual reporting on sustainability (pages 37 – 81) Finance Review Continued from previous page |

|

23 Financial ratios and operational metrics Finance Review Continued from previous page Return on assets Profit/loss from operating activities Average assets Return on equity Profit/loss for the year Average equity Equity ratio Equity, year-end Total equity and liabilities, year-end Contracted days Number of on hire days in the fiscal year (in total for all vessels), considering only 12 days in re-gards of Eneti. Utilisation Contracted days Days in the year (365*all vessels) Earnings per Share Result for the year Average number of shares during the year Diluted earnings per Share Result for the year Average number of shares during the year + average number of shares that would be issued on conver-sion of all the dilutive potential ordinary shares into ordinary shares Contract Backlog (As of reporting date) The total value of all customer contracts, both firm and options, that are not yet recognised as revenue as of the reporting date, and includes all new con-tracts signed until the same reporting date of the an-nual or interim report. Firm days are counted at full committed amounts, while options are measured at 50%. The definition also includes any contracts where revenue recognition has started but not yet completed as of the reporting date Contract Backlog (As of report release date) The total value of all customer contracts, both firm and options, that are not yet recognised as revenue as of the reporting date, but includes all new con-tracts signed until the release date of the annual or interim report. Firm days are counted at full commit-ted amounts, while options are measured at 50%. The definition also includes any contracts where rev-enue recognition has started but not yet completed as of the reporting date. |

|

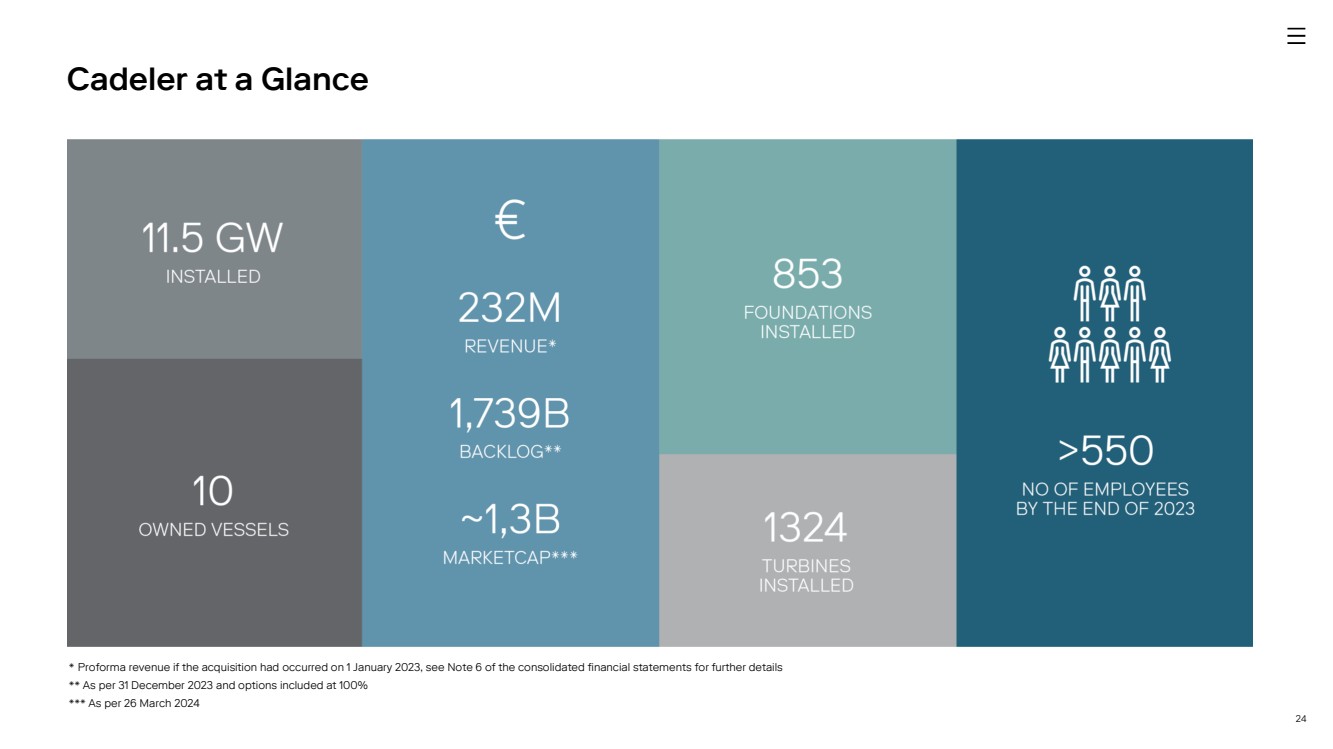

24 Cadeler at a Glance * Proforma revenue if the acquisition had occurred on 1 January 2023, see Note 6 of the consolidated financial statements for further details ** As per 31 December 2023 and options included at 100% *** As per 26 March 2024 |

|

25 The Cadeler Group is subject to various regulatory and compliance requirements under international and national maritime regulations which significantly affect the ownership and operation of the Cadeler Group’s fleet. The regulations mainly relate to marine safety, environmental protection and maritime security. The below is a description of the general regulatory framework in which the Cadeler Group operates and should not be considered exhaustive neither in respect of the subjects covered nor the details pro-vided. International Maritime Organisation Most of the regulations relating to vessel operations are based on international rules is-sued predominantly by the IMO, the United Nations (“UN”) agency for maritime safety and the prevention of pollution by vessels. The primary IMO regulations include the Inter-national Conventions for the Safety of Life at Sea (“SOLAS”), the International Conven-tion of the Standards of Training, Certification and Watchkeeping for Seafarers (“STCW”), and MARPOL. Vessel Safety and Security Requirements The SOLAS Convention was adopted in order to address the safe manning of vessels and emergency training drills. The Convention of Limitation of Liability for Maritime Claims (the “LLMC”) sets limitations of liability for a loss of life or personal injury claim or a property claim against ship owners. Under Chapter IX of the SOLAS Convention, or the International Safety Management Code for the Safe Operation of Ships and for Pollution Prevention (the “ISM Code”), the Cadeler Group’s operations are also subject to environmental standards and require-ments. The ISM Code requires the party with operational control of a vessel to develop an extensive safety management system that includes, among other things, the adop-tion of a safety and environmental protection policy setting forth instructions and proce-dures for operating its vessels safely and describing procedures for responding to emer-gencies. The IMO has also adopted the International Convention on Standards of Training, Certifi-cation and Watchkeeping for Seafarers (“STCW”). As of February 2017, all seafarers are required to meet the STCW standards and be in possession of a valid STCW certificate. The IMO’s Maritime Safety Committee and MEPC, respectively, each adopted relevant parts of the International Code for Ships Operating in Polar Water (the “Polar Code”). The Polar Code covers design, construction, equipment, operational, training, search and res-cue as well as environmental protection matters relevant to ships operating in the waters surrounding the two poles. It also includes mandatory measures regarding safety and pollution prevention as well as recommendatory provisions. The Polar Code applies to new ships constructed after 1 January 2017 and after 1 January 2018, ships constructed before 1 January 2017 are required to meet the relevant requirements by the earlier of their first intermediate or renewal survey. Decarbonisation, energy efficiency and Air Emissions MARPOL is applicable to vessels of any type under countries that are signatories and is broken into six Annexes, each of which regulates a different source of pollution. Annex I relates to oil leakage or spilling; Annexes II and III relate to harmful substances carried in bulk in liquid or in packaged form, respectively; Annexes IV and V relate to sewage and garbage management, respectively; and Annex VI, lastly, relates to air emissions. Regulatory |

|

26 Annex VI to MARPOL addresses air pollution from vessels. Annex VI sets limits on sulfur oxide and nitrogen oxide emissions from all commercial vessel exhausts and prohibits “deliberate emissions” of ozone depleting substances (such as halons and chlorofluoro-carbons), emissions of volatile compounds from cargo tanks, and the shipboard incinera-tion of specific substances. Annex VI also includes a global cap on the sulfur content of fuel oil and allows for special areas to be established with more stringent controls on sulfur emissions, as explained below. Emissions of “volatile organic compounds” from certain vessels, and the ship-board incineration (from incinerators installed after 1 January 2000) of certain substances (such as polychlorinated biphenyls, or “PCBs”) are also prohibited. Pollution Control and Liability Requirements The IMO has negotiated international conventions that impose liability for pollution in in-ternational waters and the territorial waters of the signatories to such conventions. The IMO has, inter alia, adopted an International Convention for the Control and Manage-ment of Ships’ Ballast Water and Sediments (the “BWM Convention”) in 2004. The BWM Convention requires ships to manage their ballast water to remove, render harmless, or avoid the uptake or discharge of new or invasive aquatic organisms and pathogens within ballast water and sediments. The BWM Convention’s implementing regulations call for a phased introduction of mandatory ballast water exchange requirements, to be replaced in time with mandatory concentration limits, and require all ships to carry a bal-last water record book and an international ballast water management certificate. The IMO also adopted the International Convention on Civil Liability for Bunker Oil Pollu-tion Damage (the “Bunker Convention”) to impose strict liability on ship owners (including the registered owner, bareboat charterer, manager or operator) for pollution damage in jurisdictional waters of ratifying states caused by discharges of bunker fuel. The Bunker Convention requires registered owners of ships over 1,000 gross tons to maintain insur-ance for pollution damage in an amount equal to the limits of liability under the applica-ble national or international limitation regime (but not exceeding the amount calculated in accordance with the LLMC). Anti-Fouling Requirements In 2001, the IMO adopted the International Convention on the Control of Harmful Anti-fouling Systems on Ships (the “Anti-fouling Convention”). The Anti-fouling Convention prohibits the use of organotin compound coatings to prevent the attachment of mol-luscs, anti-fouling systems containing cybutryne and other sea life to the hulls of vessels. Vessels of over 400 gross tons engaged in international voyages will also be required to undergo an initial survey before the vessel is put into service or before an International Anti-fouling System Certificate (the “IAFS Certificate”) is issued for the first time; and subsequent surveys when the anti-fouling systems are altered or replaced. International Labour Organisation The International Labour Organisation (the “ILO”) is a specialised agency of the UN that has adopted the Maritime Labor Convention 2006 (“MLC 2006”). A Maritime Labor Cer-tificate and a Declaration of Maritime Labor Compliance is required to ensure compli-ance with MLC 2006 for all ships of 500 gross tons or over and are either engaged in in-ternational voyage or flying the flag of a member and operating from a port, or between ports, in another country. Regulatory Continued from previous page |

|

27 EU Regulations Decarbonisation and energy efficiency The EU made a unilateral commitment to reduce overall greenhouse gas emissions from its member states from 20% of 1990 levels by 2020. The EU also committed to reduce its emissions by 20% under the Kyoto Protocol’s second period from 2013 to 2020. Regulation (EU) 2015/757 of the European Parliament and of the Council of 29 April 2015 (amending EU Directive 2009/16/EC) (“MRV Regulation”) governs the monitoring, report-ing and verification of carbon dioxide emissions from maritime transport, and, subject to some exclusions, requires companies with ships over 5,000 gross tonnage to monitor and report carbon dioxide emissions annually. The EU has adopted several regulations and directives requiring, among other things, more frequent inspections of high-risk ships, as determined by type, age and flag as well as the number of times the ship has been detained. The EU also adopted and extended a ban on substandard ships and enacted a minimum ban period and a definitive ban for repeated offenses. The regulation also provided the EU with greater authority and con-trol over classification societies, by imposing more requirements on classification socie-ties and providing for fines or penalty payments for organisations that failed to comply. Furthermore, the EU has implemented regulations requiring vessels to use reduced sul-fur content fuel for their main and auxiliary engines. The EU Directive 2005/33/EC (amending Directive 1999/32/EC) introduced requirements parallel to those in Annex VI relating to the sulfur content of marine fuels. In addition, the EU imposed a 0.1% maxi-mum sulfur requirement for fuel used by ships at berth in the Baltic, the North Sea and the English Channel (the so called “SOx-Emission Control Area). As of January 2020, EU member states also have to ensure that ships in all EU waters, except the SOx-Emission Control Area, use fuels with a 0.5% maximum sulfur content. On 15 September 2020, the European Parliament voted to include greenhouse gas emis-sions from the maritime sector in the EU’s carbon market, the EU ETS. On July 14, 2021, the European Commission formally proposed its plan, which would involve gradually in-cluding the maritime sector from 2024 and phasing the sector in over a three-year pe-riod. This will require shipowners to buy permits to cover these emissions. On 18 Decem-ber 2022, the Environmental Council and European Parliament agreed to include mari-time shipping emissions within the scope of the EU ETS in phases: shipping companies will pay for 40% for verified emissions from 2024, 70% for 2025 and 100% for 2026. Most large vessels will be included in the scope of the EU ETS from the start, with offshore vessels being included from 2027. Offshore vessels above 5,000 gross tonnage will be included in the EU ETS from 2027. The inclusion of general cargo vessels and offshore vessels between 400-5,000 gross tonnage in the ETS will be reviewed in 2026. Pollution Control and Liability Requirements EU Directive 2009/123/EC (amending Directive 2005/35/EC) on ship-source pollution and on the introduction of penalties for infringements imposes criminal sanctions for il-licit ship-source discharges of polluting substances, including minor discharges, if com-mitted with intent, recklessly or with serious negligence and the discharges individually or in the aggregate result in deterioration of the quality of water. Aiding and abetting the discharge of a polluting substance may also lead to criminal penalties. The directive ap-plies to all types of vessels, irrespective of their flag, but certain exceptions apply to war-ships or where human safety or that of the ship is in danger. Regulatory Continued from previous page |

|

28 Ship recycling The EU has put in place regulatory requirements on the recycling of vessels. The recy-cling of vessels is subject to various international, regional and national requirements, in-cluding the 1989 Basel Convention/EU Waste Shipment Regulation (1013/2006), the 2009 Hong Kong Convention and the EU Ship Recycling Regulation (1257/2013) which may apply depending on the vessel flag and the location of the vessel when the decision to recycle the vessel was taken. The regulations put in place certain requirements relat-ing to, inter alia, the export of vessels destined for recycling and the manner in which the recycling is carried out. Inspection by Classification Societies The hull and machinery of every commercial vessel must be classed by a classification society authorised by its country of registry. The classification society certifies that a vessel is safe and seaworthy in accordance with the applicable rules and regulations of the country of registry of the vessel and SOLAS. Most insurance underwriters make it a condition for insurance coverage and lending that a vessel be certified “in class” by a classification society which is a member of the International Association of Classification Societies, the IACS. A vessel must undergo annual surveys, intermediate surveys, drydockings and special surveys. In lieu of a special survey, a vessel’s machinery may be on a continuous survey cycle, under which the machinery would be surveyed periodically over a five-year period. Every vessel is also required to be drydocked every periodically for inspection of the un-derwater parts of the vessel. If any vessel does not maintain its class and/or fails any an-nual survey, intermediate survey, drydocking or special survey, the vessel will be unable to carry cargo between ports and will be unemployable and uninsurable and there may be further commercial consequences. Other Coastal State Requirements As a matter of international law, the coastal states are permitted, subject to certain re-strictions, to put in place requirements on the vessels’ operations in the territorial waters. Furthermore, the coastal state is entitled to exploit natural resources (such as wind power) in its exclusive economic zones and/or continental shelf subject to restrictions set out in the United Nations International Law of the Seas Convention (UNCLOS), Part II, Art. 2(2), Part V and VI (or customary international law). Internationally, coastal states have elected to put significantly different regulatory re-quirements. The local law requirements may relate to matters such as the ownership/na-tionality of the vessel, nationality and/or work permits for crew, and/or use of local port infrastructure. In the Cadeler Group’s activities, the Cadeler Group is confronted with a range of government policies that restrict international trade and protect domestic in-dustries. These protectionist measures manifest themselves mostly through cabotage laws which protect the domestic shipping industry from foreign competition and thus prevent or limit the us from operating in such countries. Examples of such measures can be found, among others, in the United States through the Merchant Marine Act of 1920 (also known as the Jones Act), as well as in many other jurisdictions. Regulatory Continued from previous page |

|

29 The Company’s corporate governance principles are based on, and in all material as-pects in compliance with, the Norwegian Code of Practice and applicable Danish law. In addition, and as a result of the listing of the Company’s American Depositary Shares on the New York Stock Exchange (the “NYSE”), the Company complies with applicable United States federal securities laws and regulations as well as the rules of the NYSE, in particular the corporate governance standards of Section 303A of the NYSE Listed Com-pany Manual, to the extent applicable to the Company as a foreign private issuer. A full copy of the Company’s corporate governance code is available on the Company’s website: https://www.cadeler.com/assets/uploads/PDFs/Investors/cadeler-corporate-governance-policy-2024.pdf Statutory CSR report To fulfil the requirement for statutory reporting on corporate responsibility cf. sections §99a and §107d of the Danish Financial Statements Act, the Company has integrated its annual sustainable development reporting into the Annual Report 2023, see pages 37 – 81. Also see pages 212-221 for the ESG Appendices, which contain KPIs and accounting practices related to Cadeler’s Statutory reporting. Corporate Governance 29 |

|

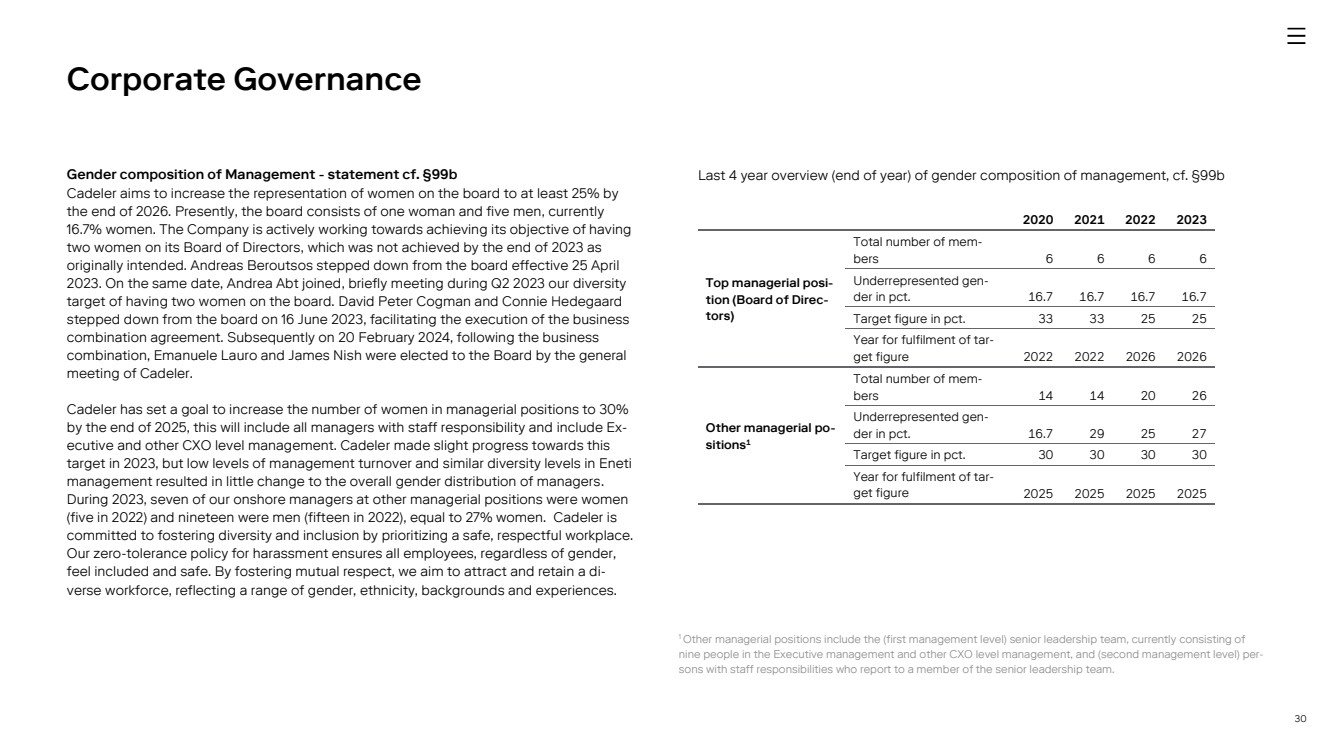

30 Gender composition of Management - statement cf. §99b Cadeler aims to increase the representation of women on the board to at least 25% by the end of 2026. Presently, the board consists of one woman and five men, currently 16.7% women. The Company is actively working towards achieving its objective of having two women on its Board of Directors, which was not achieved by the end of 2023 as originally intended. Andreas Beroutsos stepped down from the board effective 25 April 2023. On the same date, Andrea Abt joined, briefly meeting during Q2 2023 our diversity target of having two women on the board. David Peter Cogman and Connie Hedegaard stepped down from the board on 16 June 2023, facilitating the execution of the business combination agreement. Subsequently on 20 February 2024, following the business combination, Emanuele Lauro and James Nish were elected to the Board by the general meeting of Cadeler. Cadeler has set a goal to increase the number of women in managerial positions to 30% by the end of 2025, this will include all managers with staff responsibility and include Ex-ecutive and other CXO level management. Cadeler made slight progress towards this target in 2023, but low levels of management turnover and similar diversity levels in Eneti management resulted in little change to the overall gender distribution of managers. During 2023, seven of our onshore managers at other managerial positions were women (five in 2022) and nineteen were men (fifteen in 2022), equal to 27% women. Cadeler is committed to fostering diversity and inclusion by prioritizing a safe, respectful workplace. Our zero-tolerance policy for harassment ensures all employees, regardless of gender, feel included and safe. By fostering mutual respect, we aim to attract and retain a di-verse workforce, reflecting a range of gender, ethnicity, backgrounds and experiences. Last 4 year overview (end of year) of gender composition of management, cf. §99b Corporate Governance 1 Other managerial positions include the (first management level) senior leadership team, currently consisting of nine people in the Executive management and other CXO level management, and (second management level) per-sons with staff responsibilities who report to a member of the senior leadership team. 2020 2021 2022 2023 Top managerial posi-tion (Board of Direc-tors) Total number of mem-bers 6 6 6 6 Underrepresented gen-der in pct. 16.7 16.7 16.7 16.7 Target figure in pct. 33 33 25 25 Year for fulfilment of tar-get figure 2022 2022 2026 2026 Other managerial po-sitions1 Total number of mem-bers 14 14 20 26 Underrepresented gen-der in pct. 16.7 29 25 27 Target figure in pct. 30 30 30 30 Year for fulfilment of tar-get figure 2025 2025 2025 2025 |

|

31 Board of Directors Andreas Sohmen-Pao Nationality: Austrian Born: 1971 Gender: Male Joined the Cadeler board: 2021 Current election period: 2023-2025 Chairman of the Board. Considered non-independent. Other management duties, etc. ▶ BW Group Limited (Executive Chairman) ▶ BW Offshore Limited (Chairman) ▶ BW Energy Limited (Chairman) ▶ BW LPG Limited (Chairman) ▶ BW Epic Kosan Ltd (Chairman) ▶ Hafnia Limited (Chairman) ▶ Global Centre for Maritime Decarbonisation (Chairman) ▶ Lloyd’s Register Foundation (member of the Board of Trustees) Former Chairman of the Singapore Maritime Foundation, and former member of the board of Navigator Holdings Ltd. Education ▶ MBA, Harvard University, 1997 ▶ BA Honours in Oriental Studies, Oxford University 1994 Qualifications More than 20 years of experience in the shipping industry. Chairman for multiple corporate boards and board experience from interna-tional/listed companies. Attendance in Board and Committee meetings during 2023 4/4 Board meetings 4/4 Chairmanship meetings 1/1 Remuneration Committee meeting Emanuele A. Lauro Nationality: Italian Born: 1978 Gender: Male Joined the Cadeler board: 2024 Current election period: 2024-2025 Vice Chairman of the Board of Directors. Considered non-independent. Other management duties, etc. ▶ Scorpio Holdings Limited (member of the Board) ▶ Scorpio Services Holding Limited ▶ Scorpio Tankers Inc. (Chairman) ▶ Scorpio Offshore Holding Inc. ▶ Scorpio USA LLC ▶ Moxie Corp ▶ Gorgon Holdings Limited ▶ Monaco Chamber of Shipping (President) ▶ Fordham University (member of the Advisory Board) Education ▶ International Business, European Business School. Qualifications Extensive shipping industry experience spanning two decades. Chairs multiple corporate boards and active participant in the maritime com-munity and advisory boards. Attendance in Board and Committee meetings during 2023 n/a Board meetings Jesper T. Lok Nationality: Danish Born: 1968 Gender: Male Joined the Cadeler board: 2020 Current election period: 2022-2024 Board Member and chairs the Remuneration Committee. Considered independent. Other management duties, etc. ▶ Dagrofa (Chair) ▶ Evos (Chair) ▶ Gertsen & Olufsen (Chair) ▶ Inchcape Shipping Services (Chair) ▶ PISIFFIK (Vice Chair) ▶ RelyOn Nutec (Vice Chair) ▶ Silverstream Technologies (NED) ▶ TripleB (Chair) ▶ Vestergaard (Chair) Education ▶ MBA, Nova Southeastern University (NSU) Qualifications Board experience from international private and listed maritime, retail, production and services companies. Management experience as CEO in private and public companies in the maritime and mobility sectors. Attendance in Board and Committee meetings during 2023 3/4 Board meetings 1/1 Remuneration Committee meeting |

|

32 Ditlev Wedell-Wedellsborg Nationality: Danish Born: 1961 Gender: Male Joined the Cadeler board: 2020 Current election period: 2022-2024 Board Member and former chair of the Audit Committee until January 2024. Considered independent. Other management duties, etc. ▶ Wessel&Vetts Fond, (Chair) ▶ Weco Travel CEE and associated companies. (Chair) ▶ Travel House and associated companies. (Chair) ▶ Vind A/S, (Chair) ▶ Weco lnvest, (Chair) ▶ Donau Agro, (member of the Board) ▶ Damptech and associated companies, (member of the Board) ▶ AeroGuest, (member of the Board) ▶ Rigensgade Kaserne, (member of the Board) ▶ Aquitas, advisor ▶ Niki lnvest. Manager Education ▶ BA from Stanford University ▶ MBA from INSEAD Qualifications Board experience from Nordic companies and from the transporta-tion sector. Management experience from ship owning company. Attendance in Board and Committee meetings during 2023 4/4 Board meetings 5/5 Audit Committee meetings Andrea Abt Nationality: German Born: 1960 Gender: Female Joined the Cadeler board: 2023 Current election period: 2023-2025 Board Member and member of the Audit Committee. Former ob-server of the Audit Committee during 2023. Considered independent. Other management duties, etc. ▶ Energy Technology Holdings LLC / Exide Technologies (NED) ▶ Gerresheimer AG (member of the Supervisory Board) ▶ Mar Holdco S.à.r.l., Luxemburg (NED) Education ▶ English and Spanish Philology from Rheinische Friedrich-Wilhelms University, Bonn ▶ MBA from Rotman School of Management, University of Toronto Qualifications Listed and non-listed board experience in European and US compa-nies, broad executive background in a variety of functions. Specialist knowledge in procurement and logistics. Attendance in Board and Committee meetings during 2023 3/3 Board meetings 3/3 Audit Committee meetings as an Observer. James Nish Nationality: American Born: 1958 Gender: Male Joined the Cadeler board: 2024 Current election period: 2024-2025 Board Member and chair of the Audit Committee from February 2024 Considered independent. Other management duties, etc. ▶ Gibraltar Industries, Inc. (Chairman of Audit Committee and Capital Structure and Asset Management Committee) ▶ Alert360 Home Security Business (Lead Director) Education ▶ BS in Accounting and Business, State University of New York. ▶ MBA, Wharton School of the University of Pennsylvania Qualifications Over 30 years of experience in investment banking, serving clients across a variety of international industrial markets. Certified public ac-countant and adjunct professor at Baruch College, Zicklin School of Business in New York and at Pace University, Lubin. Attendance in Board and Committee meetings during 2023 n/a Board meetings n/a Audit Committee meetings |

|